This is the September 2018 investment conditions report. It includes both a written version and audio commentary.

Listen To The September 2018 Investment Conditions Audio Commentary

The audio commentary is an integral part of the Investment Conditions report as it provides additional context to the written report.

Audio Download

Data Download

The following spreadsheet contains monthly valuation, economic trends and market internal data used in the investment conditions report from December 2015 through the most recent report period.

Purpose of the Investment Conditions Report

The purpose of the monthly investment conditions report is to objectively look at market valuations, economic and central bank trends, and market internals such as price trends, momentum and investor sentiment data to determine if there is a regime change that suggests investors should make adjustments to their asset allocation and portfolio structure.

In other words, are the risks of bad times in terms of bear market losses and higher volatility increasing or decreasing.

Monitoring investment conditions is helpful for scaling exposure to risky assets such as stocks as favorable investment conditions generally align with positive investment returns while unfavorable investment conditions have generally been associated with sub-par investment returns.

In this report, investment conditions are segmented into three areas:

- Market valuations – measure how inexpensive or pricey the global stock market, bonds and other asset classes are.

- Economic and central bank trends – measure the anticipated direction of the economy based on purchasing managers indices (“PMI”) and other economic indicators and how accommodating central banks are in terms of their interest rate policies.

- Market internals – measure market trends and momentum and the level fear and greed exhibited by investors.

Market valuations, market internals and economic and central bank trends can be thought of as traffic stoplights that are each individually flashing red, green or yellow.

When all three are red as they were in early 2008, that warrants extreme caution and a more conservative investment approach.

When all three are green as they were in mid 2009 coming out of the Great Recession, then that provides an opportunity to increase portfolio risk and generate higher returns.

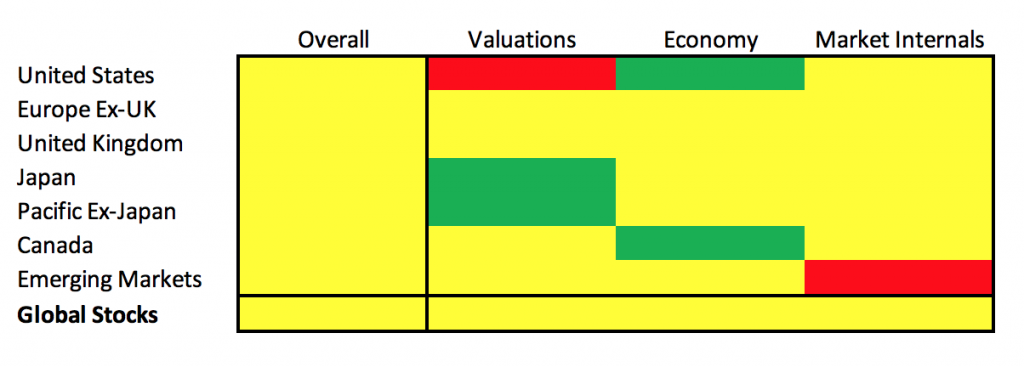

Currently, global valuations, economic trends and market internals are YELLOW with investment conditions neutral.

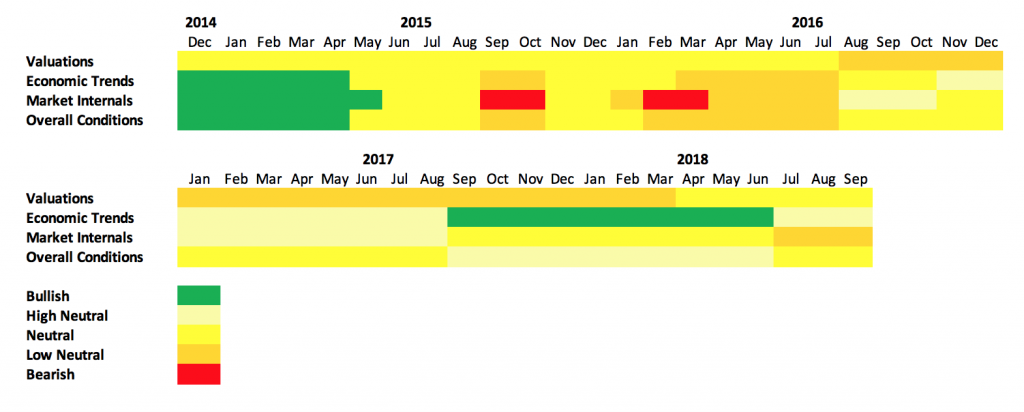

Historical Investment Conditions

Overall Global Investment Conditions Are Neutral (Yellow)

Investment conditions are neutral or YELLOW as of early September 2018. They are in the middle of the neutral range, having been downgraded from high neutral in early July as economic trends and market internals deteriorated.

Despite robust U.S. economic growth and recent new highs in the U.S. stock market, globally investment conditions are weakening. This is evident in the divergence between the capitalization weighted MSCI All Country World Index which returned 3.8% year-to-date through August and the equal weighted MSCI All Country World Index, which has returned -3.4% over the same period. The equal weighted MSCI All Country Word ex-U.S. has declined -7.1% year-to-date. The percent of global markets with rising 200 day moving averages is down to 51%, its lowest level since the U.S. presidential election in 2016.

The Global Manufacturing PMI fell by 0.2 points at the beginning of September to 52.5, its seventh decline in the last eight months. It is now at is lowest level since November 2016.

The equity allocation in the model portfolios was reduced by 5% points in early July as investment conditions deteriorated and since then economic trends and market internals have gotten worse, suggesting the next incremental change in the models is more likely to be a further decrease in the stock weight rather than an increase.

Emerging market stocks seem most vulnerable as economic trends there weaken. Flows into emerging markets over the past four weeks have been positive, providing some support for the asset class, but we will be closely monitoring ETF flows to see if the trend reverses.

Global valuations are at their long-term average, but the U.S stock market remains expensive. A high valuation for U.S. stocks will likely lead to below average returns in the decade ahead, but high valuations have not kept the U.S. stock market from being one of the world’s better performing markets in 2018 with a gain of close to 10% year-to-date.

Global valuations, economic trends and market internals are all rated YELLOW and in neutral territory as of early September 2018. This suggests investors with a long-term time horizon should keep their portfolio allocations in line with their long-term targets. However, the deterioration in economic trends and market internals also suggest investors should be cautious about increasing their exposure to stocks and other risk assets until there is more clarity on the economic and trade fronts.

It is important to recognize stock markets are part of a complex adaptive system which means unexpected market sell-offs can occur irrespective of investment conditions.

Investors should never have such a large allocation to stocks that their lifestyle or retirement plans would be seriously undermined due to unexpected severe market losses.

You can get examples of how to invest given current market conditions on the Model Portfolios page. You can find more detail on my current allocation and holdings on the Portfolio Profile page.

The remainder of the report provides an overview of market returns and more detail regarding market valuations, market internals and economic and central bank trends.

Market Returns

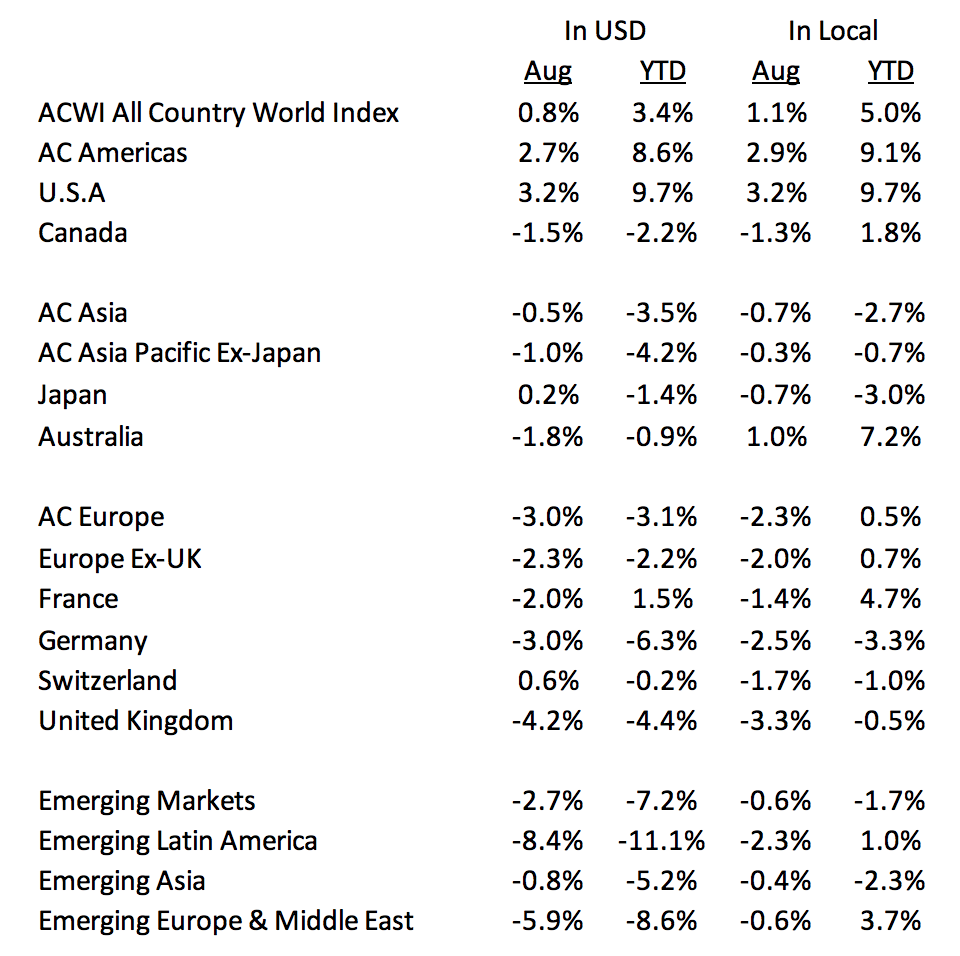

Global stocks as measured by the MSCI All Country World Index were positive in August, boosted by the strength of the U.S. stock market, which has now gained close to 10% year-to-date.

Year-to-date, the global stock market advance has been narrow with 45% of countries in positive territory year-t0-date in local currencies, but only 19% positive when year-to-date returns are quoted in U.S. dollars.

Emerging markets stocks have been the worst performing region, down 10.5% year-to-date through the first week of September as measured by the MSCI Emerging Markets Index, although a strengthening dollar has been a big contributor to the loss. In local currency terms, emerging market stocks have returned -4.4% year-to-date.

The following table provides an overview of equity market returns:

Global Stock Market Returns For the Periods Ending August 31, 2018

Source: MSCI

Bond Market and Income Strategy Returns

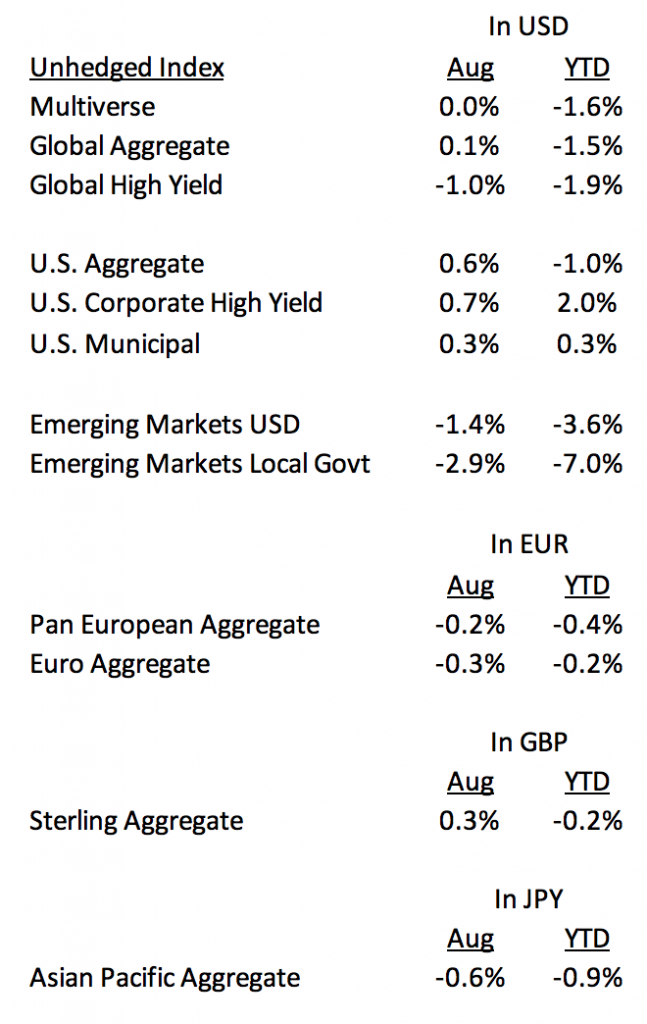

The global bond market was flat in August while U.S. bonds were slightly positive due to falling rates. Emerging market bonds were the worst performer for the month and year-to-date due to increasing yields. The Bloomberg Barclays Emerging Market Bond Index now yields 6.0%, a 1.5% point increase from the beginning of the year. The spread or incremental yield relative to 10-year Treasury bonds is 3.2%, up from 2.2% at the beginning of the year. Spreads for emerging market bonds remain below their 4.2% average going back to 1997.

The following table provides an overview of bond market returns:

Fixed Income Returns For the Periods Ending August 31, 2018

Source: Bloomberg

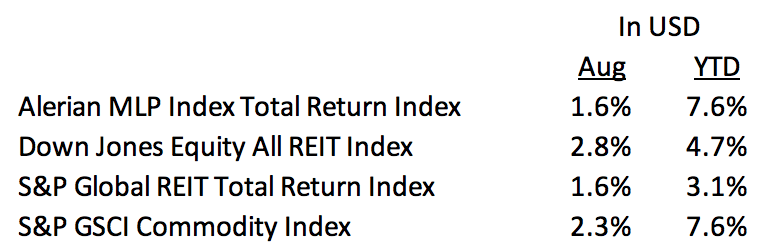

Income strategies were positive in August with real estate investment trusts and MLPs returning over 15% since March after a sell-off to start the year.

MLPs, REITs and Commodities Returns For the Periods Ending August 31, 2018

Market Valuations – YELLOW

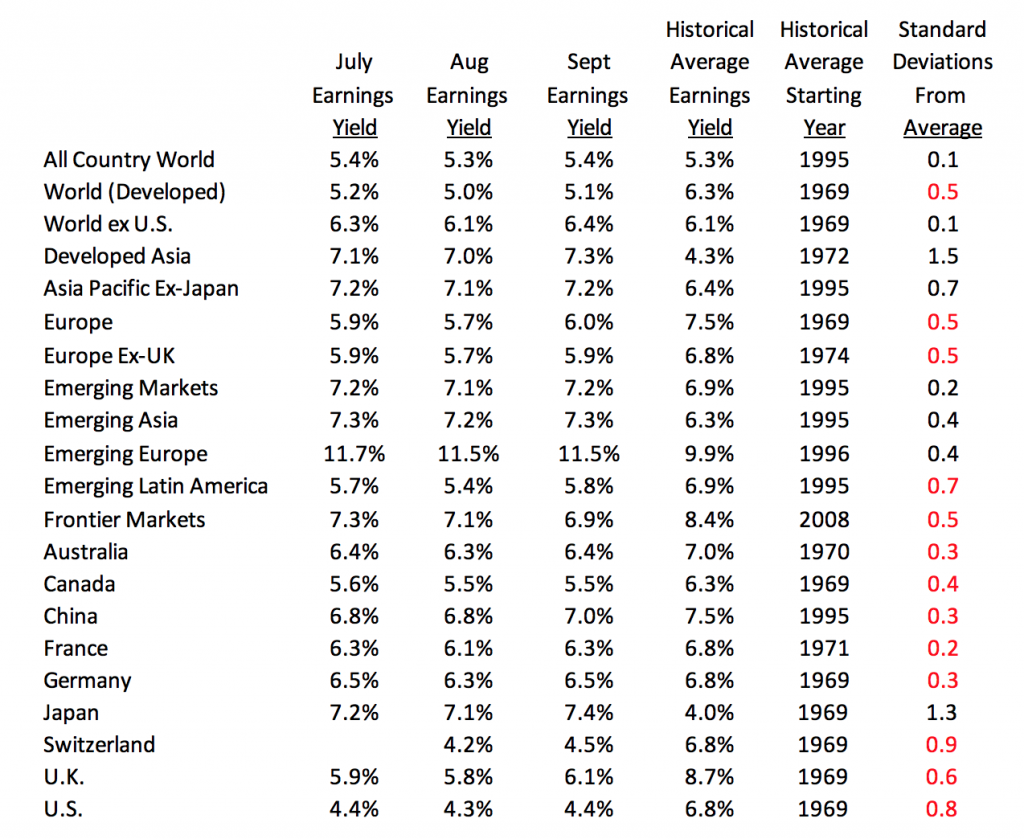

Stock market valuations remain in neutral territory with the earnings yield for the MSCI All Country World Index at 5.4%, near its 20 year average. The higher the earnings yield the more attractive the valuation.

Despite the sell-off in emerging markets stocks, their valuations remain close to their 20 year average. That contrasts to emerging markets after their sell-off in the 2013 to 2015 period where the earnings yield was over 8%, setting the stage for the strong emerging market stock performance in 2016 and 2017.

Global earnings growth remains robust with analysts anticipating U.S. and emerging markets will experience double digit earnings growth over the next year with developed non-U.S. markets expected to have earnings growth in the high single digits.

Stock buybacks continue to boost earnings per share growth.

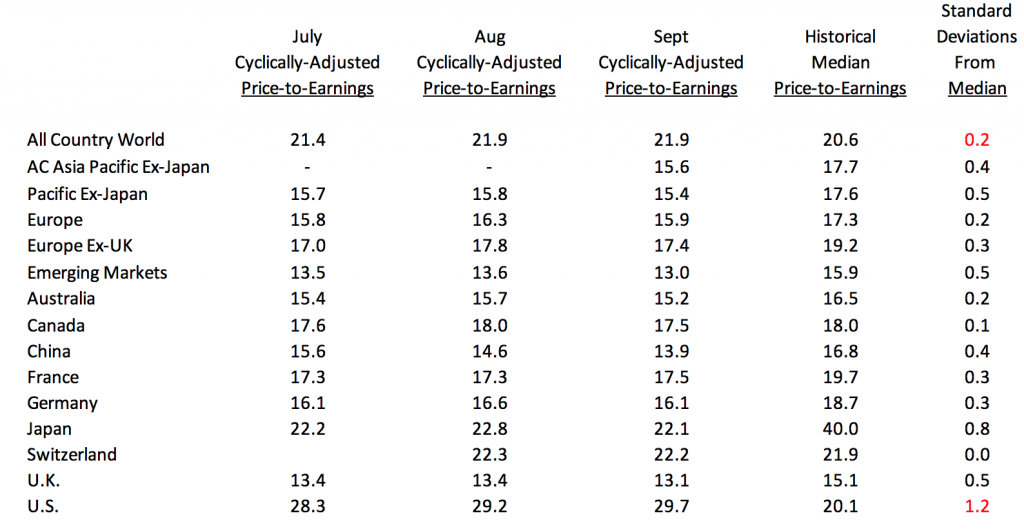

The U.S. remains the one of the most expensive stock market in the world on an earnings yield basis and as well as based on its cyclically-adjusted priced to earnings ratio. Yet, just because a stock market is expensive, does not mean it can continue to do well, as evidenced by the strong year-to-date U.S. stock market performance.

Still, extremely high valuations have been followed by lower returns in the subsequent decade. When the cyclically adjusted price-to-earnings ratio for U.S. stocks has been at its current level, 60% of the time the annualized real price return over the next decade has been negative with the median being -1.4%. This is equates to a low single digit return for U.S. stocks on a nominal basis including dividends.

Earnings Yields as of September 1, 2018

Note: The earnings yield figures are based on trailing twelve month earnings. Earnings yield is the inverse of the price-to-earnings ratio. The lower the earnings yield, the more expensive the valuation. Standard deviation measures how far outside of the norm the earnings yield is. The higher the standard deviation the further the current measure is from the average. Standard deviations listed in red denote a market that is more expensive than average while those in black are average or cheaper than average.

Source: Ned Davis Research

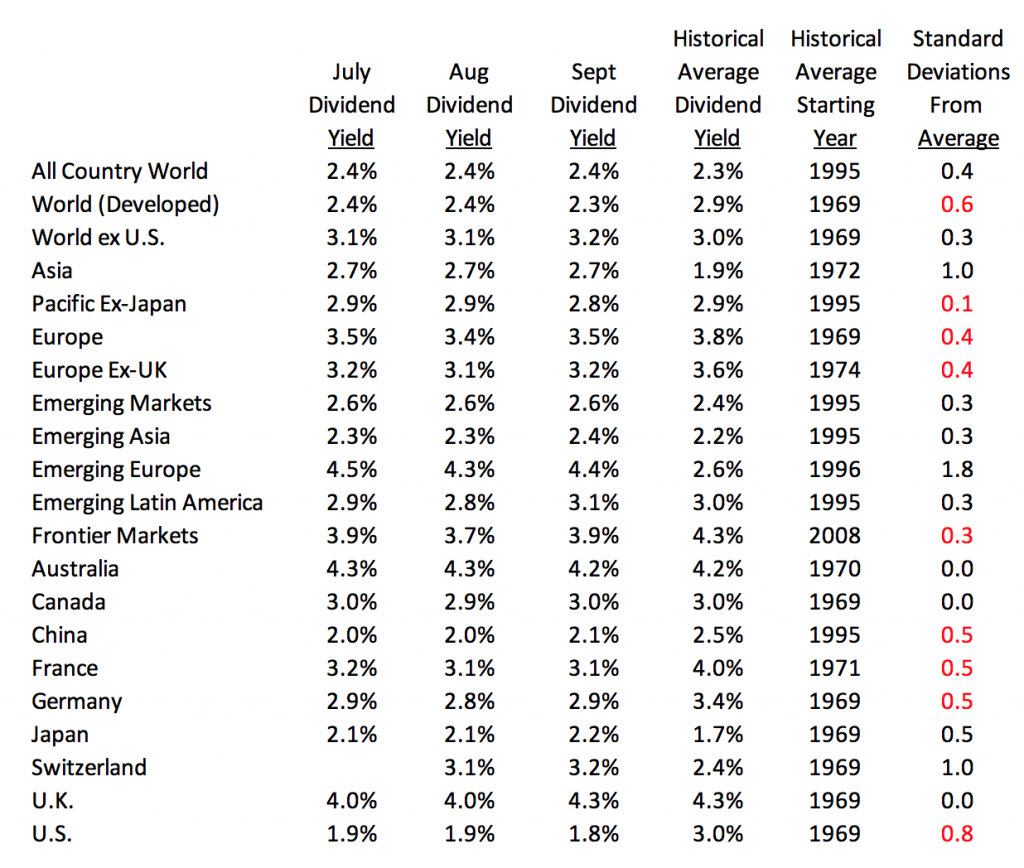

Dividend Yields as of September 1, 2018

Note: The dividend yield figures are based on trailing twelve month dividends. Standard deviation measures how far outside of the norm the dividend yield is. The higher the standard deviation the further the current measure is from the average. Standard deviations listed in red denote a market with a dividend yield lower than average while those in black are markets with dividend yields that are average or higher than average.

Source: Ned Davis Research

Equity Cyclically-Adjusted Price-to-earnings Ratios

Source: Ned Davis Research, MSCI

Note: Cyclically-adjusted P/E Ratios also known as Shiller P/E’s are based on the previous 10 year average earnings using MSCI Indices. One important consideration when making valuation judgements using 10-year earnings is whether the previous decade reflects the earnings potential going forward. In other words, are there outliers in the historical earnings record that are not repeatable? Standard deviation measures how far outside of the norm the dividend yield is. The higher the standard deviation the further the current measure is from the average. Standard deviations listed in red denote a market that is more expensive than its historical average while those in black are markets that are average or cheaper than average.

The following section provides some additional valuation metrics for select U.S. bond and income strategies.

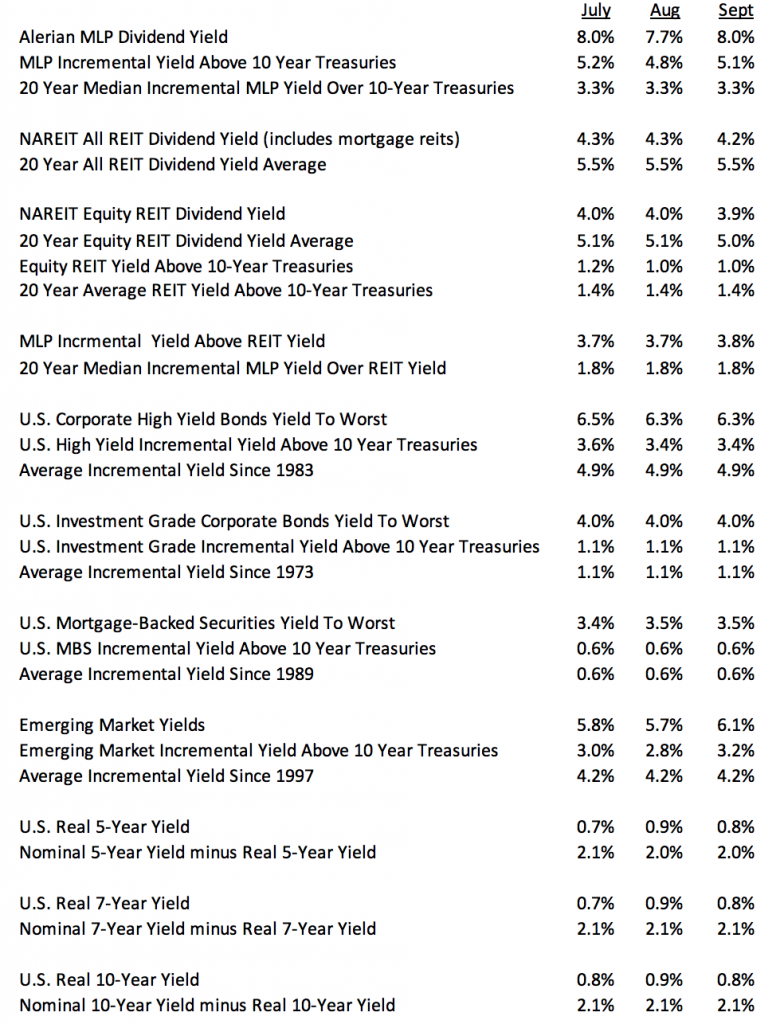

Select Bond and Income Strategy Valuations as of September 1, 2018

Source: Ned Davis Research

Despite the solid returns for MLPs on a year-to-date basis, their dividend yields at 8.0% are above their long-term average relative to 10-year Treasuries.

Given the 16% rebound in U.S. reits since March, the extreme undervaluation has narrowed. Equity REIT dividend yields have gone from yielding 1.6% more then 10 -year Treasuries in March to 1.0% today. The 20 year average spread is 1.4%.

REITs price to funds from operations, the equivalent of the P/E, is slightly below its long-term average of 16.5. Meanwhile, REITs discount to the private market value of their real estate holdings has also narrowed but continues to sell at a single digit discount.

U.S. non-investment grade and emerging market bonds remain richly valued with the incremental spread relative to U.S. Treasuries below their long-term historical averages.

Economic and Central Bank Trends – YELLOW

The most robust data set for understanding global economic growth trends is Purchasing Manager Indices (PMIs), which are monthly surveys of businesses conducted by Markit and other providers.

There are both Manufacturing and Non-Manufacturing PMI surveys conducted each month. Generally, a reading above 50 suggests an economy is expanding while a reading below 50 suggests an economy is contracting.

This report focuses on Manufacturing PMIs as they have a longer and more accurate history of predicting global recessions.

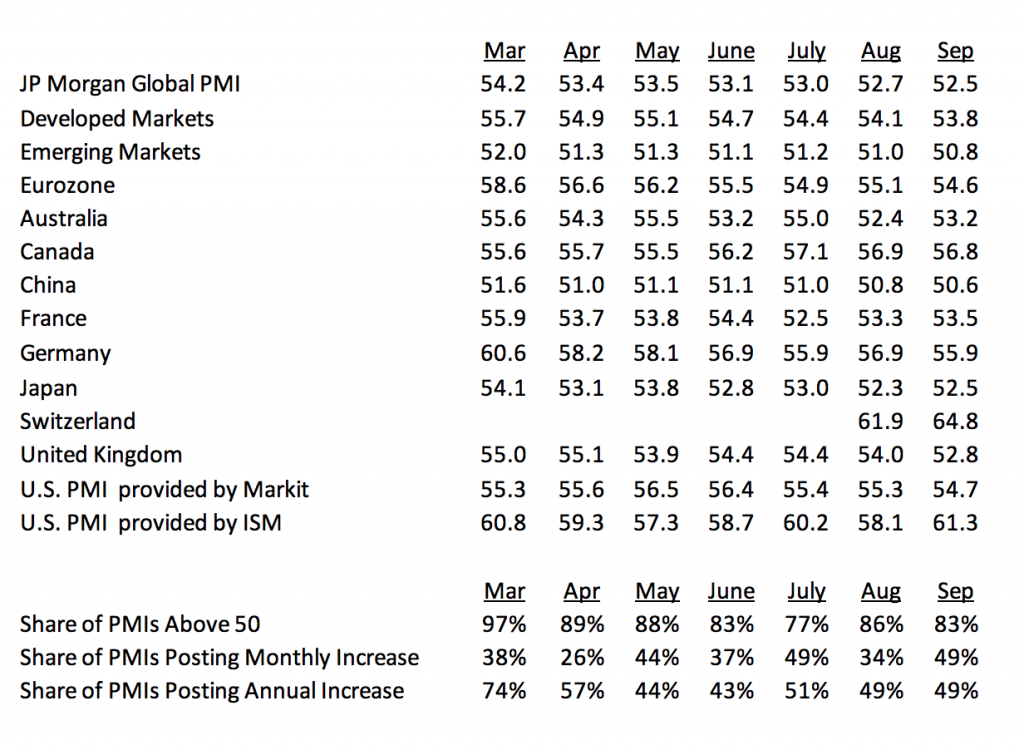

The following table provides an overview of global PMI as well as select regions and countries.

PMI Data As of September 1, 2018

Source: Markit, ISM and Ned Davis Research

The Global Manufacturing PMI fell by 0.2 points at the beginning of September to 52.5, its seventh decline in the last eight months. It is now at is lowest level since November 2016. Economic momentum has slowed but global PMI remains above its long-term average of 51.5. Still, with the new orders component at a two year low, the risk of a recession is increasing.

The majority (83%) of countries remain in expansion territory with global manufacturing PMIs greater than 50, although only half of countries showed a year-over-year increase in PMI.

Emerging markets PMI fell again to 50.8 and is just above the dividing line between expansion and contraction. Turkey and South Africa are both in contraction territory with PMIs of 46.4 and 43.4, respectively.

Economic trends are YELLOW after being downgraded from GREEN in July.

The U.S. and Europe are the leading regions in terms of PMI data, although Europe’s economic momentum has slowed, falling from over 60 at the beginning of the year to 54.6 today.

PMI for the U.S. was mixed with ISM showing an improvement while Markit showed a continued deterioration. Incoming economic data suggest the U.S. economy will continue its above trend expansion into the third quarter but not quite as strong as Q2 GDP that came in at an upwardly revised 4.2% annual rate.

The six month rate of change for the Conference Board’s Leading Index of U.S. economic indicators was 2.7%, a slight improvement 2.5% last month. 90% of the index’s underlying components were higher then six months ago. Leading economic indicators suggest the risk of a U.S. recession is extremely low.

The U.S. employment report released in early September showed 201,000 with average hourly earnings growth increasing at 2.9 year-over-year, its highest level in nine years. At this point, U.S. economic data all but guarantees the Federal Reserve will again raise its policy rate at its meeting this month and again in December.

The risk for the U.S. economy is rising interest rates start to negatively impact U.S. economic growth in 2019 as the Federal Reserve continues on its path of raising its short-term policy rate.

Market Internals – YELLOW

Market internals, such as trend, momentum, and sentiment, are fast variables since they are driven by investor emotion whereas valuations and economic trends tend to change more slowly.

At times, market internals can act as an accelerant that magnifies the prevailing long-term secular trend that is driven by valuations and economic and central bank trends.

At other times, market internals can dampen the prevailing long-term trend.

Adjusting investment portfolios based exclusively on market internals is a trading strategy that can be effective, but is not compatible with the longer-term focus of the Money For the Rest of Us Plus.

Instead, we can combine the faster variables of market internals with the slower variables of valuations and economic and central bank trends in order to identify regime changes that suggest the risk of a major equity market sell-off is high or, conversely, conditions are in place for a major equity market advance.

Market internals are essentially a swing vote that reinforces or dampens the primary message coming from the slow variables of market valuations and economic and central bank trends.

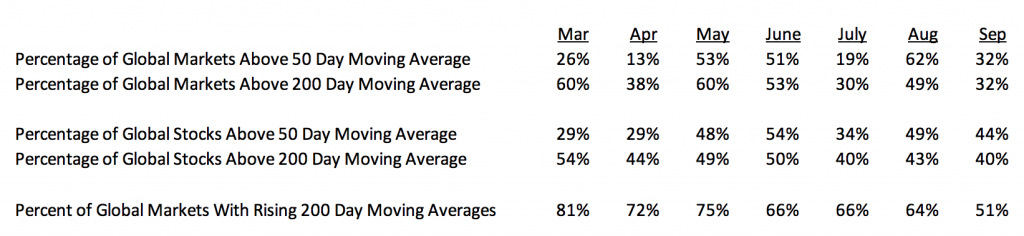

The following table provides and overview of prevailing global market trends, which measure the direction of markets:

Global Equity Market Trend Data as of September 1, 2018

Source: Ned Davis Research

Despite the U.S. stock market reaching new highs last week, overall market internals continue to deteriorate as market breadth weakens. Market internals remain in low neutral. The deterioration is most evident in the divergence between the capitalization weighted MSCI All Country World Index which returned 3.8% year-to-date through August and the equal weighted MSCI All Country World Index, which has returned -3.4% over the same period. The equal weighted MSCI All Country Word ex-U.S. has declined -7.1% year-to-date.

The percent of global markets with rising 200 day moving averages fell to 51% this month. A drop to well below 50% have been characteristic of the last three bear markets. The majority of stocks and markets remain below their 50 day and 200 day moving averages.

Momentum data, which measures the rate of change in global stocks and markets, is in the low neutral territory globally, as is investor sentiment data in terms of investor pessimism is also low neutral.

Summary

Global valuations, economic trends and market internals are rated YELLOW and in neutral territory. Overall investment conditions are YELLOW, suggesting investors with a long-term time horizon should keep their portfolio allocations in line with their long-term targets. However, the deterioration in economic trends and market internals over the past couple of months also suggest investors should be cautious about significantly increasing their exposure to stocks and other risk assets until there is more clarity on the economic and trade fronts.

The following tables provides a summary of market conditions by region.