Special Purpose Acquisition Companies or SPACs are non-operating publicly-listed companies whose purpose is to identify and purchase a private company.

How do SPACs work and are they worth investing in?

ARTICLE TABLE OF CONTENTS (Skip to Section)

What are SPACs?

Special Purpose Acquisition Companies or SPACs are non-operating publicly-listed companies whose purpose is to identify and purchase a private company, allowing the acquisition target to have publicly listed stock.

SPACs are also known as blank check companies. When a SPAC or other publicly-traded company purchases a private company, it is called a reverse merger. A traditional merger is when a private company takes a public company private.

According to SPAC Insider, in 2021, 613 newly formed SPACs raised $162 billion in capital through initial public offerings. That is double the amount of capital raised in 2020 when 248 new SPACs were formed. More SPACs were launched in 2020 and 2021 than in the prior twenty years combined.

Why SPACs Exist

You might be wondering:

Why do SPACs even exist?

Private companies are willing to be acquired by SPACs because it is more flexible and less burdensome than going public through an initial public offering (IPO).

The financial markets’ receptiveness to new public offerings varies depending on economic conditions and investors’ risk appetite. A SPAC is already public, so a reverse merger allows a private company to become public when the IPO window is closed.

SPAC acquisitions are also attractive to private companies because their founders and other major shareholders can sell a higher percentage of their ownership in a reverse merger than they would with an initial public offering.

The private company founders can also avoid the lock-up periods for selling newly public shares that are required for initial public offerings.

Become a Better Investor With Our Investing Checklist

Become a Better Investor With Our Investing Checklist

Master successful investing with our Checklist and get expert weekly insights to help you build your wealth with confidence.

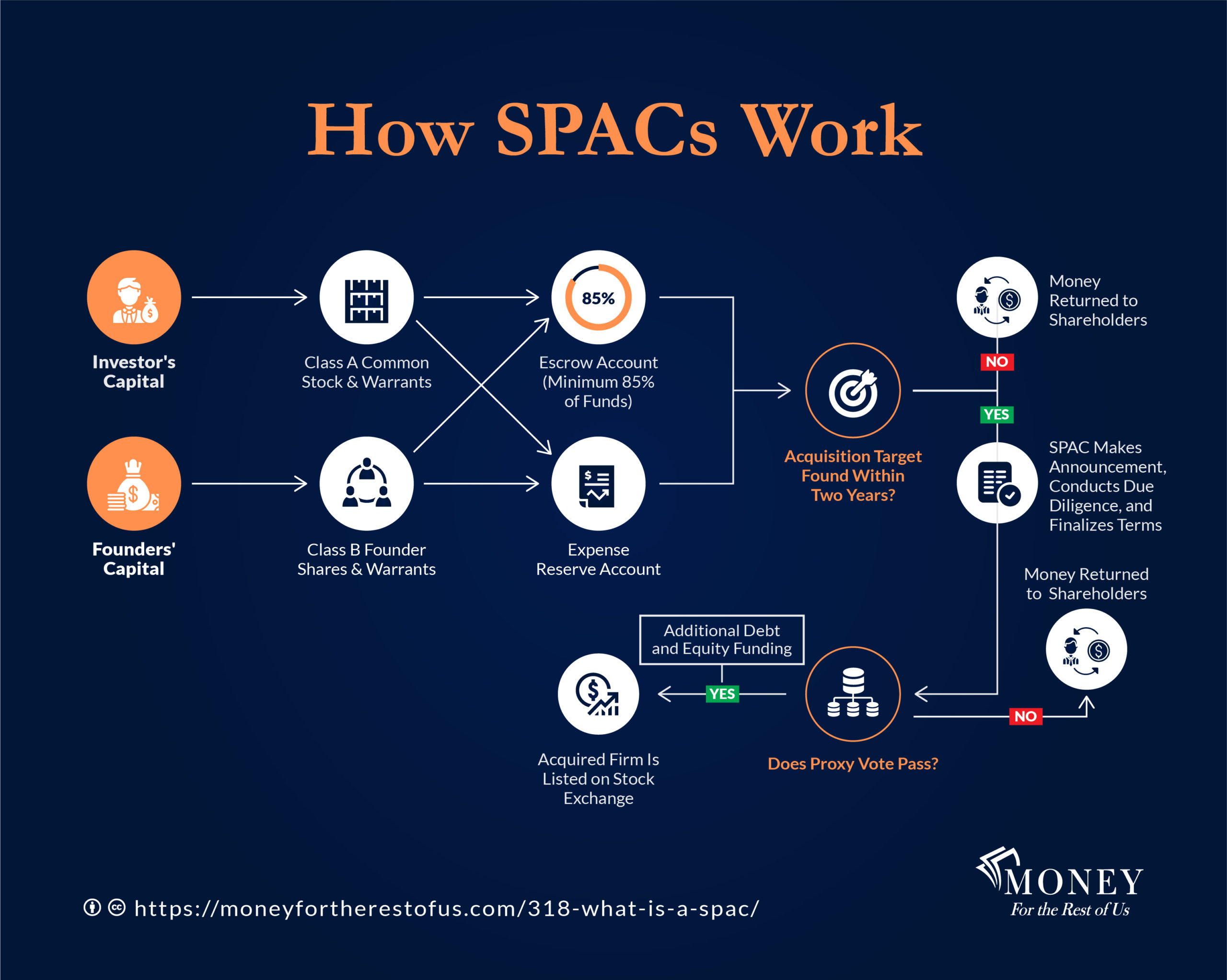

How SPACs Work

SPACs raise capital to make an acquisition through an initial public offering.

A typical SPAC IPO structure consists of a Class A common stock share combined with a warrant. A warrant gives the holder the right to buy more stock at a fixed price at a later date.

Investors who participate in the SPAC IPO are attracted to the opportunity to exercise the warrants so they can get more common stock shares once the acquisition target is identified and the transaction closes.

The typical IPO price for a SPAC common stock is $10 per share. The exercise price for the warrants is typically set about 15% or higher than the IPO price.

A few weeks after the IPO is completed the warrant is spun off and trades separately from the SPAC stock.

At least 85% of the SPAC IPO proceeds must be placed in an escrow account for a future acquisition.

In practice, closer to 97% of the capital raised goes into the escrow account, while 3% is held in reserve to cover IPO underwriting fees and SPAC operating expenses, including due diligence, legal, and accounting fees.

Funds in the escrow account are usually invested in government bonds.

After the IPO, the SPAC’s management team searches for a potential acquisition target. During this period, the SPAC stock should trade near its IPO price since the proceeds are held in government bonds, although during market sell-offs, SPAC stocks can fall below the IPO price.

SPACs can also trade at a premium to the IPO price if shareholders believe management will identify a compelling acquisition target.

SPACs have a specified period to identify an acquisition target and close the deal. The time period is usually two years.

If the SPAC sponsor cannot close an acquisition within the given time period, then the money in the escrow account is returned to the shareholders.

If the SPAC sponsors identify a potential target firm, they make a formal announcement. The day the public is notified about the potential acquisition is called the announcement date.

“I have never found any blank-check investment vehicle attractive, no matter what the reputation or what the sponsor might be…. They are the ultimate in terms of lack of transparency.”

– Arthur Levitt, former SEC Chairman

After the announcement, the SPAC sponsors perform additional due diligence and negotiate the acquisition structure. The U.S. Securities and Exchange Commission also reviews the acquisition terms.

The next step is a proxy vote. The SPAC shareholders vote on whether they approve or disapprove of the acquisition. Shareholders also elect whether they want to liquidate their shares in the SPAC for a pro-rata portion of what remains in the trust account.

If a majority of shareholders approve the acquisition then it goes through as long as the number of shareholders who vote to liquidate is below a specified threshold outlined in the proxy statements.

Historically, this percentage was 20%, however, it can be as high as 30% or more.

If more than 50% disapprove of the business combination, then the escrow account is closed, and the proceeds are returned to the shareholders.

SPACs typically target companies about two to four times the amount that was raised in the initial public offering. So, to close the deal, SPACs need additional capital from outside investors. This additional capital is also needed because some of the existing SPAC shareholders would have voted to redeem their shares, taking a portion of the trust proceeds.

SPACs raise both equity and debt to complete the business combination. The equity often comes from leveraged buyout firms, in what is known as Private Investment in Public Equity or PIPEs.

Once the business combination is approved and the additional capital raised, then the transaction closed and the acquired firm is listed on the stock exchange.

SPAC Criticisms and Poor Performance

A primary criticism of SPACs is the large stock allocation the SPAC sponsors receive as part of the SPAC IPO.

These Class B Founder Shares and warrants are purchased for a nominal amount but entitle the management to up to 20% of the total stock shares outstanding following the IPO.

It gets worse:

Not only do these founders’ shares dilute Class A common stockholders, but the promote can lead to a conflict of interest as the sponsors have significant upside if they close a transaction even if the particular opportunity is not overly compelling.

These misaligned incentives have caught the attention of the U.S. Securities and Exchange Commission.

SPAC investing has been less profitable for individual investors. Most SPACs underperform the stock market and eventually fall below the IPO price.

Former SEC Chairman Jay Clayton said, “One of the areas in the SPAC space I’m particularly focused on and my colleagues are particularly focused on is the incentives and compensation to the SPAC sponsors. How much of the equity do they have now? How much of the equity do they have at the time of the IPO-like transaction? What are their incentives?”

Some recent SPAC IPOs have sought to reduce the conflict of interest and shareholder dilution.

For example, Pershing Square Tontine Holdings, led by billionaire hedge fund manager Bill Ackman structured its IPO so that the sponsor purchased $1 billion of stock along with some warrants. Pershing Square expects the dilution to Class A stockholders to be only 6% compared to the typical 20%.

Become a Better Investor With Our Investing Checklist

Become a Better Investor With Our Investing Checklist

Master successful investing with our Checklist and get expert weekly insights to help you build your wealth with confidence.

Poor SPAC Performance

SPAC performance has been subpar and could be even worse going forward given the amount of capital that has been raised as SPACs compete with each other for target companies, potentially overpaying.

Academics Johannes Kolb and Tereza Tykvova analyzed the performance of SPACs that went public between 2013 and 2015.

After adjusting for size and industry, they found that SPACs not only lagged the overall stock market but underperformed traditional IPOs.

The Financial Times also analyzed SPAC performance and found most traded below their IPO prices, underperforming the overall stock market.

The authors wrote, “The poor investment record of many SPACs is a reminder than when Wall Street pushes a new product, clever financiers invariably find a way to shift most of the risk onto ordinary investors—even if a new generation of SPAC founders believes they will avoid the problems of the past.”

Data compiled by Jay Ritter, Professor of Finance at the University of Florida, shows that the average three-year return for SPACS after they have completed an acquisition is -57%.

“The fact that there are so many SPACs out there searching for mergers certainly allows an operating company to play them off against each other.”

– Jay Ritter, Professor of Finance, University of Florida

How to Invest in SPACs

Investors can invest in SPACs either by selecting individual securities or by investing in a SPAC ETF.

Selecting individual SPACs allows investors to focus on the opportunities that seem most promising while also having some downside protection due to the structure of SPACs.

Because SPAC IPO proceeds are invested in government bonds until a merger is closed, shareholders have the opportunity to exit the SPAC either through liquidation or by selling shares in the secondary market.

Consequently, SPACs are unlikely to fall much below the IPO price until after a merger is closed.

Investors that participate in the SPAC IPO receive both common stock and a warrant. A strategy often pursued by hedge funds is to sell the SPAC after the IPO and keep the warrant that could increase in value if the SPAC stock approaches or exceeds the strike price at which the warrant could be exercised for common stock shares of the SPAC.

Academics Tim Jenkinson and Miguel Sousa identified a profitable way to invest in SPACs. Their strategy was to purchase the SPAC shortly after the IPO and sell it one week after the announcement date when the potential merger was announced. The median return for this strategy was 7.6%.

My Experience Investing in SPACs

I initiated a SPAC investing experiment on December 31, 2020 based on Jenkinson and Sousa’s work. I opened an account at Robinhood and purchased 60 SPACs that were trading near their IPO price of $10 per share.

I sold each SPAC holding after the acquisition was announced and rolled the proceeds into a new SPAC. I closed out the experiment in December 2021. Overall, my SPAC portfolio broke even. Gains were positive in January 2021 as many SPACs traded at a premium to the IPO price, but gradually most fell to just below the IPO price. Rarely did the SPACs jump in price after an acquisition was announced.

I also found tracking the individual SPACS to be overly demanding.

SPAC ETFs

An active ETF that seeks to invest in the most promising SPACs is the SPAC and New Issue ETF (SPCX), managed by Tuttle Tactical Management. The fund only invests in new issue SPACs and is able to purchase some at the IPO price. The ETF intends to sell its SPACs holdings after a business combination is announced or after the SPAC shares rise in price.

The ETF was launched in December 2020 and has $17 million in assets under management. The expense ratio is 0.95%. The ETF owns 121 individual SPACs. The ETF has returned -1.7% annualized since its inception in 2020.

Conclusion

In 2020 and 2021, a number of prominent investors and media personalities launched SPACs or are considering doing so.

For example, former NBA basketball legend Shaquille O’Neal, along with three former Disney executives and one of Martin Luther King Jr.’s sons, plan to launch a SPAC that targets technology and media companies.

Other prominent figures that have plans to lead SPACs or are already doing so are former U.S. House of Representatives Speaker Paul Ryan, and Oakland Athletics executive Billy Beane, who was featured in the film and book Moneyball.

A successful SPAC acquisition can lead to a windfall for the SPAC sponsors because as part of the IPO they get to purchase up to 20% of the outstanding shares for a nominal amount of money.

SPAC investing has been less profitable for individual investors. Most SPACs underperform the stock market and eventually fall below the IPO price. Given SPAC’s poor track record, most investors should be wary of investing in them.

Become a Better Investor With Our Investing Checklist

Become a Better Investor With Our Investing Checklist

Master successful investing with our Checklist and get expert weekly insights to help you build your wealth with confidence.

Podcast Episode 318: What Are SPACs and Should You Invest in Them?

Topics covered include:

- How much money has been raised in SPAC initial public offerings and who are some of the better known sponsors

- What are the benefits of a SPAC acquisition compared to a traditional initial public offering

- How SPACs work from the initial IPO to the acquisition of a private company

- How have SPACs performed so poorly

- How a new SPAC ETF is structured

- An intriguing way to invest in SPACs that potentially could outperform

Show Notes

Almost everything you need to know about SPACs by Connie Loizos—Tech Crunch

Nikola Corp to go public at over $3.3 billion valuation by Reuters Staff—Reuters

A SPAC ETF Makes Its Debut Today. Here Is What You Need to Know. by Nicholas Jasinski—Barron’s

Serial Entrepreneurs: Evidence from SPACs by Kristi Marvin, Tereza Tykvova, and Milos Vulanovic

Episode Sponsors

Tempo – Use code David to save $100

Learn More

253: Are IPOs the New Ponzi Scheme?

219: The Incredible Shrinking Stock Market

436: Revisiting Carbon, SPACs, Silver, Convertible Bonds, and Frontier Markets

Transcript

As a Money For the Rest of Us Plus member, you are able to listen to the podcast in an ad-free format and have access to the written transcript for each week’s episode. For listeners with hearing or other impairments that would like access to transcripts please send an email to jd@moneyfortherestofus.com Learn More About Plus Membership »

David Stein is the founder of Money for the Rest of Us. Since 2014, he has produced and hosted the Money for the Rest of Us investing podcast. The podcast reaches tens of thousands of listeners per episode and has been nominated for ten Plutus Awards and won one. David also leads Money for the Rest of Us Plus, a premium investment education platform that provides professional-grade portfolio tools and training to over 1,000 individual investors. He is the author of Money for the Rest of Us: 10 Questions to Master Successful Investing, which was published by McGraw-Hill. Previously, David spent over a decade as an institutional investment advisor and portfolio manager. He was a managing partner at FEG Investment Advisors, a $15 billion investment advisory firm. At FEG, David served as Chief Investment Strategist and Chief Portfolio Strategist.

Become a Better Investor With Our Investing Checklist

Become a Better Investor With Our Investing Checklist

Master successful investing with our Checklist and get expert weekly insights to help you build your wealth with confidence.