This is the May 2015 investment conditions report and market exposure recommendation. It includes both a written version and audio commentary.

Listen To The May 2015 Investment Conditions Audio Commentary

Audio Download

May 2015 Investment Conditions

Favorable investment conditions can be thought of as favorable weather. Just as you don’t launch a sail boat when heavy storms are likely, there are favorable investing conditions when the sun is shining and there is a tailwind that raises the likelihood of positive portfolio returns.

Monitoring investment conditions is helpful for scaling exposure to risky assets such as stocks as favorable investment conditions generally align with positive investment returns while unfavorable investment conditions have generally been associated with sub-par investment returns.

Still, stock markets are part of a complex adaptive system which means unexpected market sell-offs can occur irrespective of investment conditions.

Investors should never have such a large allocation to stocks that their lifestyle or retirement plans would be seriously undermined due to an unexpected market losses.

Market Returns

The global stock market generated strong returns in April in U.S. dollar and local currency terms. It remains positive year-to-date.

The U.S. dollar index weakened for the month so equity market benchmarks generally did better in U.S. dollar terms than they did when priced in local currency.

The following table provides an overview of equity market returns by region.

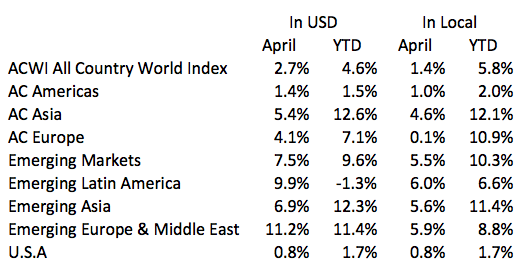

MSCI All Country World Index Returns For the Periods Ending April 30, 2015

Source: MSCI

63% of the countries (i.e. 29 out of 46) that comprise the MSCI All Country World Index posted positive returns for the month in local currency terms.

87% of the countries (i.e. 40 out of 46) that comprise the MSCI All Country World Index achieved positive returns year-to-date in local currency terms.

Hungary is the best performing market year-to-date, gaining 43% while Greece is the worst performer declining 17%.

Bond Market Returns

The weakening U.S. dollar led to a decline in the Barclays Global Aggregate Bond Index when priced on an unhedged basis.

On a hedged basis, the Global Aggregate declined in April. The Index remains positive year-to-date on an unhedged basis but negative when unhedged, reflecting the weakening euro relative to the dollar.

Both U.S. and European bonds fell in April as interest rates rose. Both regions remain positive year-to-date.

The following provides an overview of bond market returns.

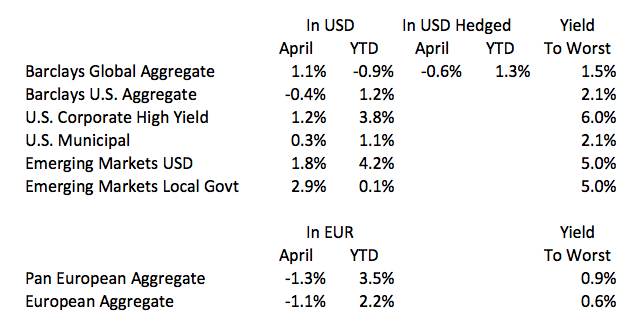

Fixed Income Returns For the Periods Ending April 30, 2015

Source: Barclays

Long-term treasuries were the worst performing U.S bond sector for the month, declining 3.1%. They have gained 0.7% year-to-date.

High yield bonds were the best performing sector in April as non-investment grade bonds gained 1.2%. High yield has returned 3.8% year-to-date.

Investment Recommendations

Investment conditions for global stocks are modestly favorable. Market Internals are rated GREEN while valuations and economic/central bank trends are rated YELLOW.

This is a change from last month as economic trends were lowered from GREEN to YELLOW as economic growth appears to be slowing.

While the secular bull market remains in place, the risk of a cyclical sell off has increased somewhat as valuations have risen, economic growth appears to be slowing and we are moving into the late spring/early summer months when seasonality trends are more neutral.

Currently, when combining valuations, market internals and economic/central bank trends no one region be it Europe, Asia, North America or Emerging Markets stands out as particularly attractive or vulnerable relative to each other.

Consequently, my portfolio remains diversified across regions with a particular focus on those countries that are most attractive from a valuation/market internal perspective.

You can get more detail on my current allocation and holdings on my Portfolio Profile page.

Investors should maintain a weighting in stocks modestly above their long-term equity target allocation.

The following report divides investment conditions into three areas:

1. Market Valuations

2. Market Internals

3. Economic and Central Bank Trends

Market valuations, market internals and economic and central bank trends can be thought of as traffic stoplights that are each individually flashing red, green or yellow.

When all three are red as they were in September 2008, that warrants extreme caution and a more conservative investment approach. With only one area green (market internals) and two yellow, investors should have moderate exposure to risky assets.

Here is a review of each segment:

Market Valuations – YELLOW

The strong performance in European and Asian stocks year-to-date combined with only moderate corporate profit growth has led to more expensive market valuations. Market valuations have been progressively increasing since the last cyclical bear market that occurred in 2011.

The most expensive markets on a valuation basis are in Europe while emerging markets have the most attractive valuations relative to other regions, although emerging markets are in line with their historical average.

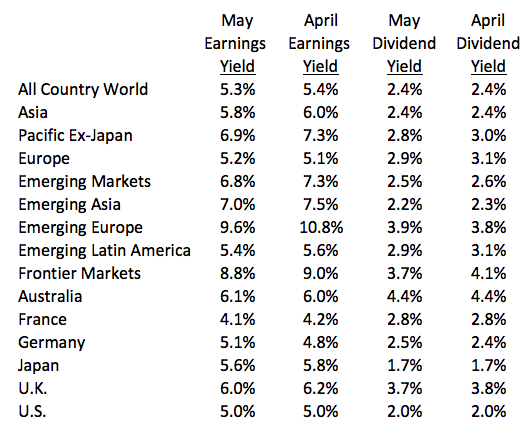

The following table provides an overview of valuations for various regions and select countries. The higher the yield in terms of earnings and dividends, the more attractive the valuation.

Valuations as of May 1, 2015

Source: Ned Davis Research

Market Internals – GREEN

Market valuations are helpful in assessing the long-term potential for stocks, but they are not particularly useful in determining market direction in the short to intermediate time frames.

Markets can stay overvalued for long periods of time and investors can leave a lot of money on the table if they rely exclusively on asset class valuations to determine their investment strategy.

Market internals, on the other hand, when combined with market valuations are useful for determining stock market performance over shorter time periods.

Market internals include market trends (i.e. its direction), momentum (i.e. the velocity of change) and sentiment (the level of fear and greed).

Global market internals remain strongly positive as the breadth of the current market advance is wide spread.

67% of global stock markets are above their 50-day moving down slightly from 70% last month.

When more than 50% of global stock markets are above their 50 day moving average the MSCI AC World Index has returned 11.0% per annum versus -13.2% per annum when more 50% of global stock markets are below their 50 day moving average.

83% of global stock markets are above their 200 day moving average compared with 73% last month. 71% of stock markets have rising 200 day moving averages, up from 67% last month.

When each of these indicators is above 50%, the MSCI AC World Index has gained in the high single digits. (See this video lesson for more information on 200 day moving averages as a measure of market internals).

Momentum and trend data of stocks that comprise the MSCI indices are also positive. Global stocks as measured by the MSCI All Country World Index are neither overbought or oversold.

Economic and Central Bank Trends – YELLOW

The most robust data set for understanding global economic growth trends is Purchaser Manager Indices (PMIs), which are monthly surveys of businesses conducted by Markit and other providers.

There are both Manufacturing and Services PMI surveys conducted each month. Generally, a reading above 50 suggests an economy is expanding while a reading below 50 suggests an economy is contracting.

For purposes of this report, I focus on Manufacturing PMIs as they have a longer and more accurate history of predicting global recessions.

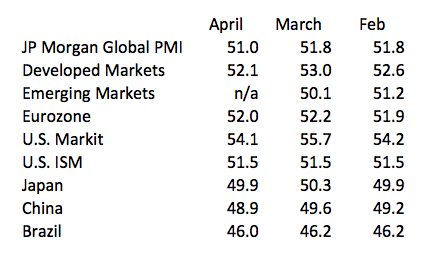

The following table provides an overview of global PMI as well as select region and countries.

PMI Data As of May 4, 2015

Source: Markit and ISM

The pace of global economic growth moderated in April. The JPM Global PMI composite index declined to 51.0 in April, a 21 month low and is now below its long-term average of 51.4.

Across the globe, the number of countries in expansion mode with PMI’s above 50 continues to decline. In April, it was 53.3%, down from 57% in March and 63% in February.

Only 30% of countries showed a positive month over month PMI increase in April down from 57% in March.

33% of countries show positive year-to-year changes in PMI, up slightly from 31% last month.

Eurozone and U.S. PMI held steady in the low 50s while Japan, China and Brazil are in contraction territory with PMI’s below 50.

Central banks remain accommodative throughout the world.

Summary

With market internals GREEN and valuations and economic/central bank trends YELLOW investment conditions are less favorable than last month but still consistent with maintaining a modestly above average exposure to higher risk, more volatile assets such as stocks.

Sources: Markit, MSCI, Ned Davis Research and ISM