This is the March 2019 investment conditions report. It includes both a written version and audio commentary.

Executive Summary

- March 9, 2019 marks the tenth anniversary of the secular bull market in stocks that began March 9, 2009. Over that ten-year period global stocks as measured by the MSCI All Country World Index returned 11.4% annualized and U.S. stocks as measured by the MSCI U.S. Index returned 15.1% annualized.

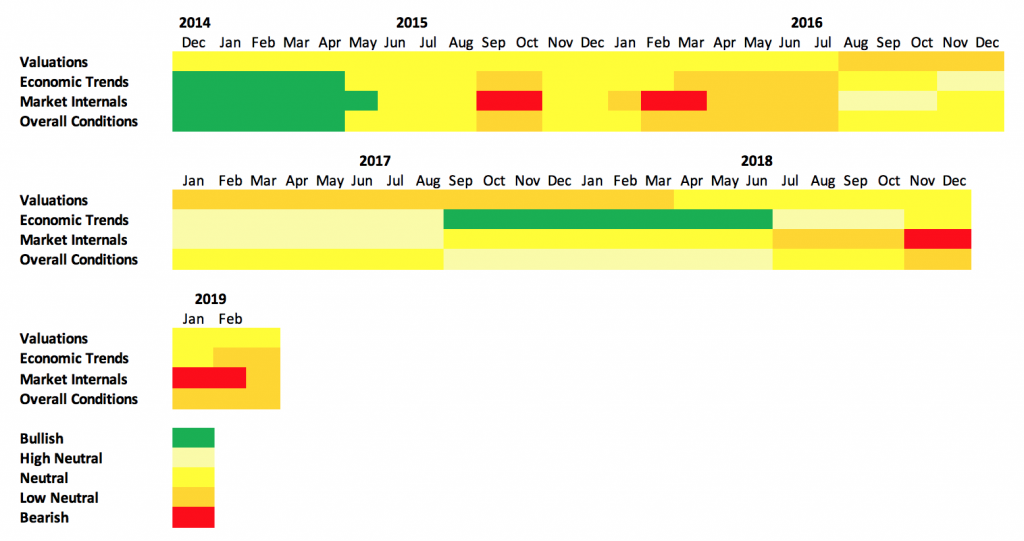

- Investment conditions are in low neutral in YELLOW territory as of early March 2019. Despite the rebound in global stocks, high yield bonds and other risks assets year-to-date, there has been little improvement in fundamental trends.

- Economic growth continues to weaken as measured by manufacturing PMI data, earnings growth expectations continue to be lowered and the percentage of companies with positive earnings revision continues to fall.

- On the valuation front, global stocks remain less expensive than their long-term average.

- Given the rebound in stocks, market internals have improved sufficiently to return to low neutral YELLOW territory from RED, although in the past two week market internals have plateaued, albeit at a neutral level.

- The December 24, 2018 low did not reach the degree of panic and capitulation of previous market sell-offs. One could be more confident that the worse market losses were behind us if economic and earnings indicators were improving instead of deteriorating. Still, with investment conditions YELLOW, in neutral territory, investors should be neither overly bearish or bullish. Investors should be patient like the Federal Reserve in observing how conditions evolve in the coming weeks and months to decide if they should be making adjustments to their asset allocation and portfolio structure.

Listen To The March 2019 Investment Conditions Audio Commentary

The audio commentary is an integral part of the Investment Conditions report as it provides additional context to the written report.

Audio Download

Data Download

The following spreadsheet contains monthly valuation, economic trends, and market internal data used in the investment conditions report from December 2015 through the most recent report period.

Purpose of the Investment Conditions Report

The purpose of the monthly investment conditions report is to objectively look at market valuations, economic and central bank trends, and market internals such as price trends, momentum and investor sentiment data to determine if there is a regime change that suggests investors should make adjustments to their asset allocation and portfolio structure.

In other words, are the risks of bad times in terms of bear market losses and higher volatility increasing or decreasing.

Monitoring investment conditions is helpful for scaling exposure to risky assets such as stocks as favorable investment conditions generally align with positive investment returns while unfavorable investment conditions have generally been associated with sub-par investment returns.

In this report, investment conditions are segmented into three areas:

- Market valuations – measure how inexpensive or pricey the global stock market, bonds and other asset classes are.

- Economic and central bank trends – measure the anticipated direction of the economy based on purchasing managers indices (“PMI”) and other economic indicators and how accommodating central banks are in terms of their interest rate policies.

- Market internals – measure market trends and momentum and the level fear and greed exhibited by investors.

Market valuations, market internals and economic and central bank trends can be thought of as traffic stoplights that are each individually flashing red, green or yellow.

When all three are red as they were in early 2008, that warrants extreme caution and a more conservative investment approach.

When all three are green as they were in mid 2009 coming out of the Great Recession, then that provides an opportunity to increase portfolio risk and generate higher returns.

Historical Investment Conditions

Overall Global Investment Conditions Are Low Neutral (Yellow)

March 9, 2019 marks the tenth anniversary of the secular bull market in stocks that began March 9, 2009. Over that ten-year period global stocks as measured by the MSCI All Country World Index returned 11.4% annualized and U.S. stocks as measured by the MSCI U.S. Index returned 15.1% annualized.

That compares to the secular bear market that ran from March 2000 to March 2009, a period when global stocks returned -7.2% annualized and U.S. stocks -8.4% annualized.

A secular bull market is a multi-year period of stock market appreciation that follows a major market bottom. It is usually characterized by extremely attractive valuations such as the greater than 10% earnings yield on the MSCI All Country World Index in March 2009.

A secular bear market is a multi-year period of sub-par stock market returns that follows a major market top. It is usually characterized by extremely expensive valuations such as earnings yields of less than 3% for the MSCI All Country World Index in March 2000.

Secular bull and bear markets include shorter-term uptrends and downtrends called cyclical bull markets and cyclical bear markets. Determining when secular and cyclical bull and bear markets start and end is easy to do in hindsight. Determining where we stand today is more difficult. We have to consider valuations, economic trends and market internals. In the monthly investment conditions report we review that data in order to decide if bear market risk is increasing or decreasing and whether we should make any portfolio adjustments. Portfolio changes should be made incrementally as we can never be completely certain of the market direction. The investment conditions reports also provide more clarity as to which asset classes are attractively priced relative to their historical averages.

As of early March 2019, investment conditions are in low neutral in YELLOW territory. Global stocks, high yield bonds, and other risks assets have rebounded from their lows on December 24, 2018, but the lack of improvement in overall economic trends makes it difficult to feel confident that a new cyclical bull within the secular bull has begun.

Economic growth continues to weaken as measured by manufacturing PMI data. Expectations for earnings growth continue to be lowered and the percentage of companies with positive earnings revision continues to fall.

The underlying economic trends appear sufficiently disconcerting to the Federal Reserve that it made a surprising U-turn at the January open market committee meeting by abandoning its plan to gradually raise its short-term policy rate.

The European Central Bank also announced this week that it would not be raising its policy rate in 2019. ECB President Mario Draghi described the current economic climate as “continued weakness” and “pervasive uncertainty.”

Given the rebound in stocks, market internals have improved sufficiently to return to low neutral YELLOW territory from RED, although in the past two weeks market internals have plateaued, albeit at a neutral level.

While it is possible that December 24, 2018, was the low and the start of cyclical bull market advance, the degree of panic and capitulation did not reach the extent of the previous seven global market sell-offs going back to 1990, according to data from Ned Davis Research. There has also been a lack of follow through in terms of U.S. investor inflows into equity mutual funds and ETFs.

One could be more confident that the worse was behind us in terms of market losses if economic and earnings indicators were improving instead of deteriorating. Still, investment conditions remain YELLOW, in neutral territory, suggesting investors should be neither overly bearish or bullish. Investors should be patient (just like the Federal Reserve) in observing how investment conditions evolve in the coming weeks and months to determine whether they should be decreasing or increasing their portfolio risk as reflected in their portfolio asset allocation.

Complex Adaptive Systems

It is important to recognize stock markets are part of a complex adaptive system which means unexpected market sell-offs can occur irrespective of investment conditions.

Investors should never have such a large allocation to stocks that their lifestyle or retirement plans would be seriously undermined due to unexpected severe market losses.

You can get examples of how to invest given current market conditions on the Model Portfolios page You can find more detail on David’s current allocation and holdings on the Portfolio Profile page.

The remainder of the report provides an overview of market returns and more detail regarding market valuations, market internals and economic and central bank trends.

Market Returns

Global stocks advanced in February and have now returned double digits year-to-date.

The following table provides an overview of equity market returns:

Global Stock Market Returns For the Periods Ending February 28, 2019

| In USD | In Local | ||||

|---|---|---|---|---|---|

| Feb | YTD | Feb | YTD | ||

| ACWI All Country World Index | 2.7% | 10.8% | 3.1% | 10.5% | |

| AC Americas | 3.1% | 11.9% | 3.1% | 11.6% | |

| U.S.A | 3.3% | 11.7% | 3.3% | 11.7% | |

| Canada | 2.8% | 16.2% | 3.1% | 12.0% | |

| AC Asia | 1.2% | 8.1% | 2.3% | 8.8% | |

| AC Asia Pacific Ex-Japan | 2.3% | 9.8% | 3.0% | 9.7% | |

| Japan | 0.0% | 6.1% | 2.3% | 7.6% | |

| Australia | 3.4% | 10.8% | 5.9% | 9.6% | |

| AC Europe | 3.1% | 10.1% | 3.4% | 9.3% | |

| Europe Ex-UK | 3.4% | 10.0% | 4.2% | 10.7% | |

| France | 4.1% | 10.2% | 4.9% | 10.7% | |

| Germany | 1.7% | 8.5% | 2.5% | 8.9% | |

| Switzerland | 4.2% | 10.6% | 4.6% | 11.8% | |

| United Kingdom | 3.4% | 10.7% | 2.3% | 6.0% | |

| Emerging Markets | 0.2% | 9.0% | 1.1% | 8.3% | |

| Emerging Latin America | -3.7% | 10.7% | -1.7% | 7.1% | |

| Emerging Asia | 1.7% | 9.1% | 1.9% | 9.3% | |

| Emerging Europe & Middle East | -2.1% | 7.4% | -1.3% | 5.3% | |

Source: MSCI

Bond Market and Income Strategy Returns

Bond markets were mixed in February with interest rates rising in some regions, leading to falling bond prices. Yields on high yields bonds fell, resulting in positive returns for the month.

The following table provides an overview of bond market returns:

Fixed Income Returns For the Periods Ending February 28, 2019

| In USD | ||

|---|---|---|

| Unhedged Index | Feb | YTD |

| Multiverse | -0.5% | 1.2% |

| Global Aggregate | -0.6% | 0.9% |

| Global High Yield | 1.4% | 5.8% |

| U.S. Aggregate | -0.1% | 1.0% |

| U.S. Corporate High Yield | 1.7% | 6.3% |

| U.S. Municipal | 0.5% | 1.3% |

| Emerging Markets USD | 0.8% | 4.0% |

| Emerging Markets Local Govt | -0.9% | 2.8% |

| In EUR | ||

| Feb | YTD | |

| Pan European Aggregate | -0.1% | 0.9% |

| Euro Aggregate | 0.1% | 1.5% |

| In GDP | ||

| Feb | YTD | |

| Sterling Aggregate | -0.7% | 0.5% |

| In JPY | ||

| Feb | YTD | |

| Asian Pacific Aggregate | 0.5% | 1.1% |

Source: Bloomberg

Real estate investment trusts and MLPs were flat to slightly positive for the month while a jump in oil prices contributed to positive returns for commodities. All three asset categories have returned double digits year-to-date.

REITs MLPs and Commodities Returns For the Periods Ending February 28, 2019

| In USD | ||

|---|---|---|

| Feb | YTD | |

| Alerian MLP Index Total Return Index | 0.3% | 12.9% |

| Down Jones Equity All REIT Index | 0.6% | 12.2% |

| S&P Global REIT Total Return Index | 0.0% | 11.0% |

| S&P GSCI Commodity Index | 3.8% | 13.1% |

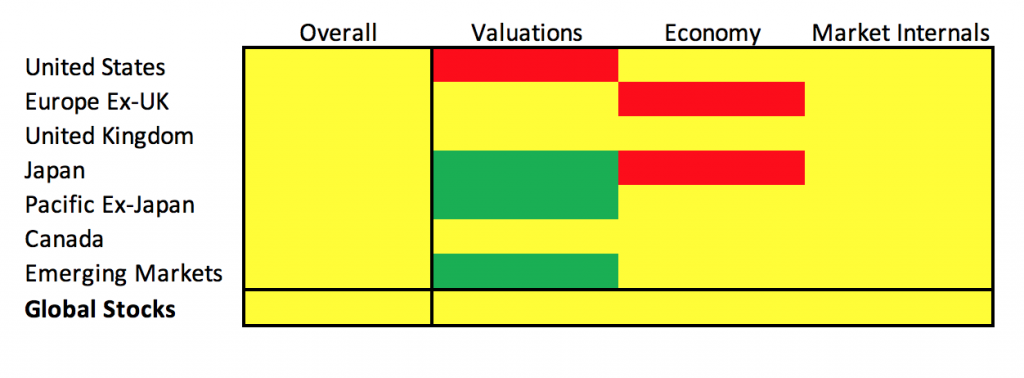

Market Valuations – YELLOW

Market valuations are neutral and in YELLOW territory. Despite the market rebound year-to-date, global stocks remain less expensive than their long-term average as measured by earnings yield and dividend yields. The higher the earnings yield the cheaper the valuation.

Global earnings expectations continue to diminish with lower expected earnings growth and a lower percentage of companies with positive earnings revisions. One year expected forward earnings growth is 6.3% for the MSCI All Country World Index and 6.1% MSCI U.S. Index. Global earnings expectations have declined sharply in the past six months where expectations had been for double-digit earnings growth. Only 56% of global companies had their earnings expectations revised upward compared to 75% a year ago. 65% of U.S. companies have positive earnings revisions compared to 87% a year ago.

The U.S. remains one of the most expensive stock markets in the world on an earnings yield basis and as measured by the cyclically-adjusted price to earnings ratio, although valuations have improved as the U.S market sold off.

Earnings Yields as of March 1, 2019

| Jan Earnings Yield | Feb Earnings Yield | Mar Earnings Yield | Historical Average Earnings Yield | Historical Average Starting Year | Standard Deviations From Average | |

|---|---|---|---|---|---|---|

| All Country World | 6.5% | 6.1% | 5.9% | 5.3% | 1995 | 0.5 |

| World (Developed) | 6.2% | 5.8% | 5.7% | 6.3% | 1969 | 0.3 |

| World ex U.S. | 7.5% | 7.1% | 6.8% | 6.1% | 1969 | 0.4 |

| Developed Asia | 8.3% | 7.9% | 7.4% | 4.3% | 1972 | 1.6 |

| Asia Pacific Ex-Japan | 8.2% | 7.7% | 7.5% | 6.4% | 1995 | 0.9 |

| Europe | 7.1% | 6.7% | 6.6% | 7.5% | 1969 | 0.3 |

| Europe Ex-UK | 6.9% | 6.6% | 6.4% | 6.8% | 1974 | 0.3 |

| Emerging Markets | 8.3% | 7.8% | 7.8% | 6.9% | 1995 | 0.7 |

| Emerging Asia | 8.5% | 8.0% | 7.8% | 6.3% | 1995 | 0.7 |

| Emerging Europe | 14.4% | 13.6% | 13.7% | 9.9% | 1996 | 0.9 |

| Emerging Latin America | 6.0% | 5.4% | 5.8% | 6.9% | 1995 | 0.9 |

| Frontier Markets | 8.0% | 7.6% | 7.6% | 8.4% | 2008 | 0.4 |

| Australia | 7.2% | 6.9% | 6.6% | 7.0% | 1970 | 0.2 |

| Canada | 6.4% | 6.0% | 5.8% | 6.4% | 1969 | 0.2 |

| China | 8.4% | 7.8% | 7.6% | 7.5% | 1995 | 0.2 |

| France | 7.0% | 6.7% | 6.6% | 6.6% | 1971 | 0.0 |

| Germany | 8.1% | 7.7% | 7.4% | 6.8% | 1969 | 0.4 |

| Japan | 8.7% | 8.3% | 7.6% | 4.0% | 1969 | 1.5 |

| Switzerland | 5.2% | 4.9% | 4.8% | 6.8% | 1969 | 0.7 |

| U.K. | 7.5% | 7.2% | 7.1% | 8.7% | 1969 | 0.3 |

| U.S. | 5.4% | 5.1% | 5.0% | 6.8% | 1969 | 0.6 |

Source: Ned Davis Research

Note: The earnings yield figures are based on trailing twelve month earnings. Earnings yield is the inverse of the price-to-earnings ratio. The lower the earnings yield, the more expensive the valuation. Standard deviation measures how far outside of the norm the earnings yield is. The higher the standard deviation the further the current measure is from the average. Standard deviations listed in red denote a market that is more expensive than average while those in black are average or cheaper than average.

Dividend Yields as of March 1, 2019

| Jan Dividend Yield | Feb Dividend Yield | Mar Dividend Yield | Historical Average Dividend Yield | Historical Average Starting Year | Standard Deviations From Average | |

|---|---|---|---|---|---|---|

| All Country World | 2.8% | 2.6% | 2.6% | 2.3% | 1995 | 0.7 |

| World (Developed) | 2.8% | 2.6% | 2.5% | 2.9% | 1969 | 0.4 |

| World ex U.S. | 3.7% | 3.5% | 3.4% | 3.0% | 1969 | 0.5 |

| Asia | 3.1% | 3.0% | 2.9% | 1.9% | 1972 | 1.4 |

| Pacific Ex-Japan | 3.3% | 3.0% | 2.9% | 2.9% | 1995 | 0.2 |

| Europe | 4.0% | 3.8% | 3.7% | 3.8% | 1969 | 0.1 |

| Europe Ex-UK | 3.7% | 3.5% | 3.4% | 3.6% | 1974 | 0.2 |

| Emerging Markets | 2.9% | 2.8% | 2.7% | 2.4% | 1995 | 0.7 |

| Emerging Asia | 2.6% | 2.5% | 2.4% | 2.2% | 1995 | 0.7 |

| Emerging Europe | 4.8% | 4.6% | 4.6% | 2.6% | 1996 | 1.9 |

| Emerging Latin America | 3.3% | 3.0% | 3.2% | 2.9% | 1995 | 0.4 |

| Frontier Markets | 4.1% | 3.9% | 3.9% | 4.3% | 2008 | 0.3 |

| Australia | 4.9% | 4.7% | 4.6% | 4.2% | 1970 | 0.4 |

| Canada | 3.5% | 3.2% | 3.2% | 3.0% | 1969 | 0.3 |

| China | 2.4% | 2.2% | 2.1% | 2.5% | 1995 | 0.4 |

| France | 3.6% | 3.4% | 3.3% | 4.0% | 1971 | 0.4 |

| Germany | 3.5% | 3.3% | 3.3% | 3.4% | 1969 | 0.1 |

| Japan | 2.6% | 2.4% | 2.4% | 1.7% | 1969 | 0.9 |

| Switzerland | 3.4% | 3.2% | 3.1% | 2.4% | 1969 | 1.0 |

| U.K. | 5.0% | 4.7% | 4.7% | 4.3% | 1969 | 0.5 |

| U.S. | 2.2% | 2.1% | 2.0% | 3.0% | 1969 | 0.7 |

Source: Ned Davis Research

Note: The dividend yield figures are based on trailing twelve month dividends. Standard deviation measures how far outside of the norm the dividend yield is. The higher the standard deviation the further the current measure is from the average. Standard deviations listed in red denote a market with a dividend yield lower than average while those in black are markets with dividend yields that are average or higher than average.

Equity Cyclically-Adjusted Price-to-earnings Ratios as of March 1, 2019

| Jan Cyclically-Adjusted Price-to-Earnings | Feb Cyclically-Adjusted Price-to-Earnings | Mar Cyclically-Adjusted Price-to-Earnings | Historical Median Price-to-Earnings | Standard Deviations From Median | |

|---|---|---|---|---|---|

| All Country World | 19.2 | 20.8 | 21.3 | 20.6 | 0.1 |

| AC Asia Pacific Ex-Japan | 14.1 | 15.2 | 15.5 | 17.6 | 0.4 |

| Pacific Ex-Japan | 14.2 | 15.2 | 15.7 | 17.4 | 0.4 |

| Europe | 14.4 | 15.4 | 15.9 | 17.2 | 0.2 |

| Europe Ex-UK | 15.6 | 16.7 | 17.3 | 19.2 | 0.3 |

| Emerging Markets | 12.3 | 13.5 | 13.4 | 15.7 | 0.4 |

| Australia | 13.6 | 14.6 | 14.9 | 16.4 | 0.3 |

| Canada | 15.1 | 17.1 | 17.6 | 17.9 | 0.0 |

| China | 12.6 | 14.0 | 14.5 | 16.6 | 0.3 |

| France | 15.7 | 16.7 | 17.6 | 19.6 | 0.2 |

| Germany | 13.8 | 14.8 | 15.1 | 18.6 | 0.4 |

| Japan | 19.6 | 20.9 | 20.7 | 38.9 | 0.8 |

| Switzerland | 20.3 | 21.5 | 22.3 | 21.9 | 0.1 |

| U.K. | 12.0 | 12.9 | 13.3 | 15.0 | 0.4 |

| U.S. | 27.3 | 27.3 | 28.1 | 20.2 | 1.0 |

Source: Ned Davis Research, MSCI

Note: Cyclically-adjusted P/E Ratios also known as Shiller P/E’s are based on the previous 10 year average earnings using MSCI Indices. One important consideration when making valuation judgements using 10-year earnings is whether the previous decade reflects the earnings potential going forward. In other words, are there outliers in the historical earnings record that are not repeatable? Standard deviation measures how far outside of the norm the dividend yield is. The higher the standard deviation the further the current measure is from the average. Standard deviations listed in red denote a market that is more expensive than its historical average while those in black are markets that are average or cheaper than average.

Select Bond and Income Strategy Valuations as of March 1, 2019

The following section reviews the absolute yield and the incremental yield or spread for bond and income oriented strategies. The comparisons allow you to see whether the spread is higher or lower than its long-term average. An asset category is more attractive when its spread is wider than its long-term average and less attractive when the spread is narrower than its long-term average.

| Jan | Feb | Mar | |

|---|---|---|---|

| Alerian MLP Dividend Yield | 9.1% | 7.9% | 7.9% |

| MLP Incremental Yield Above 10 Year Treasuries | 6.4% | 5.2% | 5.1% |

| 20 Year Median Incremental MLP Yield Over 10-Year Treasuries | 3.4% | 3.4% | 3.4% |

| NAREIT All REIT Dividend Yield (includes mortgage reits) | 4.8% | 4.3% | 4.3% |

| 20 Year All REIT Dividend Yield Average | 5.5% | 5.5% | 5.4% |

| NAREIT Equity REIT Dividend Yield | 4.4% | 3.9% | 3.9% |

| 20 Year Equity REIT Dividend Yield Average | 5.0% | 5.0% | 4.9% |

| Equity REIT Yield Above 10-Year Treasuries | 1.7% | 1.3% | 1.2% |

| 20 Year Average REIT Yield Above 10-Year Treasuries | 1.4% | 1.4% | 1.4% |

| MLP Incrmental Yield Above REIT Yield | 4.3% | 3.5% | 3.5% |

| 20 Year Median Incremental MLP Yield Over REIT Yield | 1.8% | 1.8% | 1.8% |

| U.S. Corporate High Yield Bonds Yield To Worst | 8.0% | 6.9% | 6.5% |

| U.S. High Yield Incremental Yield Above 10 Year Treasuries | 5.1% | 4.2% | 3.9% |

| Average Incremental Yield Since 1983 | 4.9% | 4.9% | 4.9% |

| U.S. Bank Loan (i.e., Leveraged Loan) Yield | 6.8% | 6.4% | 6.0% |

| U.S. Bank Loan Yield Above 3 month Eurodollar Yield | 4.0% | 3.7% | 3.4% |

| Average Incremental Yield Since 2012 | 4.4% | 4.4% | 4.4% |

| U.S. Investment Grade Corporate Bonds Yield To Worst | 4.2% | 3.9% | 3.9% |

| U.S. Investment Grade Incremental Yield Above 10 Year Treasuries | 1.4% | 1.2% | 1.2% |

| Average Incremental Yield Since 1973 | 1.1% | 1.1% | 1.1% |

| U.S. Mortgage-Backed Securities Yield To Worst | 3.5% | 3.4% | 3.4% |

| U.S. MBS Incremental Yield Above 10 Year Treasuries | 0.6% | 0.6% | 0.7% |

| Average Incremental Yield Since 1989 | 0.6% | 0.6% | 0.6% |

| Emerging Market Yields | 6.1% | 5.5% | 5.5% |

| Emerging Market Incremental Yield Above 10 Year Treasuries | 3.4% | 3.0% | 2.8% |

| Average Incremental Yield Since 1997 | 4.1% | 4.1% | 4.1% |

| U.S. Real 5-Year Yield | 1.0% | 0.7% | 0.7% |

| Nominal 5-Year Yield minus Real 5-Year Yield | 1.5% | 1.7% | 1.8% |

| U.S. Real 7-Year Yield | 1.0% | 0.8% | 0.7% |

| Nominal 7-Year Yield minus Real 7-Year Yield | 1.6% | 1.8% | 1.9% |

| U.S. Real 10-Year Yield | 1.0% | 0.8% | 0.8% |

| Nominal 10-Year Yield minus Real 10-Year Yield | 1.7% | 1.9% | 1.9% |

| U.S. 10-Year Treasury Yield | 2.7% | 2.6% | 2.7% |

Source: Ned Davis Research

Economic and Central Bank Trends – YELLOW

The most robust data set for understanding global economic growth trends is Purchasing Manager Indices (PMIs), which are monthly surveys of businesses conducted by Markit and other providers.

There are both Manufacturing and Non-Manufacturing PMI surveys conducted each month. Generally, a reading above 50 suggests an economy is expanding while a reading below 50 suggests an economy is contracting.

This report focuses on Manufacturing PMIs as they are more cyclical have a longer and more accurate history of predicting global recessions.

The following table provides an overview of global PMI as well as select regions and countries.

PMI Data As of March 1, 2019

| Sep | Oct | Nov | Dec | Jan | Feb | Mar | |

|---|---|---|---|---|---|---|---|

| JP Morgan Global PMI | 52.5 | 52.2 | 52.1 | 52.0 | 51.5 | 50.7 | 50.6 |

| Developed Markets | 53.8 | 53.6 | 53.4 | 52.8 | 52.3 | 51.8 | 50.4 |

| Emerging Markets | 50.8 | 50.3 | 50.5 | 50.8 | 50.3 | 49.5 | 50.6 |

| Eurozone | 54.6 | 53.2 | 52.0 | 51.8 | 51.4 | 50.5 | 49.3 |

| Australia | 53.2 | 54.0 | 54.5 | 54.6 | 54.0 | 53.9 | 52.9 |

| Canada | 56.8 | 54.8 | 53.9 | 54.8 | 53.6 | 53.0 | 52.6 |

| China | 50.6 | 50.0 | 50.2 | 50.2 | 49.7 | 48.3 | 49.9 |

| France | 53.5 | 52.5 | 51.2 | 50.8 | 49.7 | 51.2 | 51.5 |

| Germany | 55.9 | 53.7 | 52.2 | 51.8 | 51.5 | 49.7 | 47.6 |

| Japan | 52.5 | 52.5 | 52.9 | 52.2 | 52.6 | 50.3 | 48.9 |

| Switzerland | 64.8 | 59.7 | 57.4 | 57.7 | 57.8 | 54.3 | 55.4 |

| United Kingdom | 52.8 | 53.8 | 51.1 | 53.2 | 54.2 | 52.8 | 52.0 |

| U.S. PMI provided by Markit | 54.7 | 55.6 | 55.7 | 55.3 | 53.8 | 54.9 | 53.0 |

| U.S. PMI provided by ISM | 61.3 | 59.8 | 57.7 | 59.3 | 54.1 | 56.6 | 54.2 |

| Sep | Oct | Nov | Dec | Jan | Feb | Mar | |

|---|---|---|---|---|---|---|---|

| Share of PMIs Above 50 | 83% | 88% | 79% | 74% | 71% | 69% | 63% |

| Share of PMIs Posting Monthly Increase | 49% | 40% | 36% | 54% | 35% | 26% | 40% |

| Share of PMIs Posting Annual Increase | 49% | 29% | 36% | 20% | 15% | 14% | 14% |

Source: Markit, ISM and Ned Davis Research

Economic trends are YELLOW and remain in low neutral after having been downgraded last month. The JP Morgan Global Manufacturing PMI fell to 50.6 as of early March, its lowest level since June 2016. Only 63% of countries worldwide are in expansion territory, and 86% of countries have seen their PMI weaken over the past 12 months. The global manufacturing PMI has fallen for ten consecutive months, its longest streak of declines since December 2008.

For the first time since 2013, emerging market PMIs are higher than developed markets, but both developed and emerging market PMIs are near economic stagnation levels. They have not yet deteriorated to a level that suggests a global economic recession is imminent.

The global manufacturing output sub-component fell to 50.7 its lowest level in 32 months, while the new orders subcomponent held at 50.1, its lowest level in six years.

U.S. manufacturing PMI deteriorated in March with both Markit and ISM showing a drop. Economic trends in the U.S. have been downgraded to YELLOW from GREEN as leading indicators have deteriorated. The six-month rate of change for the Conference Board’s Leading Index of U.S. economic indicators was 0.8%, its lowest in two years. 60% of the index’s underlying components were higher than six months ago, also a two year low. Despite the downgrade, leading economic indicators suggest the risk of a U.S. recession remains low, but the risk is higher than a month ago. U.S. recessions are typically preceded by the six-month rate of change for the Conference Board’s Leading Index declining by at least 2% and more than 80% of the leading index underlying components lower than the six months prior.

One positive on the economic front is the U.S. services PMI rebounded to 59.7. This contributed to the global services PMI reaching 53.3. The composite global manufacturing and services PMI is at 52.6, up from 52.1 last month. During global recessions such as 2008 and 2001, the composite global PMI fell below 48.

The bottom line is global manufacturing growth continues to slow, but with services rebounding, the risk of a global recession is low to moderate. Overall economic trends are low neutral and in YELLOW territory.

In terms of central bank trends, the U.S. Federal Reserve remains on hold regarding future interest rate hikes. The weak U.S. March employment report will keep the Fed on hold. With only 20,000 new jobs created in February, the six month average gain for U.S. employment is 190,000, the weakest in over a year.

The European Central Bank announced it would not increase its policy rate until at least next year after cutting its estimate for European economic growth to 1.1% in 2019 down from 1.7%.

Central bank policy is more accommodative than it was at the beginning of the year.

Market Internals – RED

Market internals, such as trend, momentum, and sentiment, are fast variables since they are driven by investor emotion whereas valuations and economic trends tend to change more slowly.

At times, market internals can act as an accelerant that magnifies the prevailing long-term secular trend that is driven by valuations and economic and central bank trends.

At other times, market internals can dampen the prevailing long-term trend.

Adjusting investment portfolios based exclusively on market internals is a trading strategy that can be effective, but is not compatible with the longer-term focus of the Money For the Rest of Us Plus.

Instead, we can combine the faster variables of market internals with the slower variables of valuations and economic and central bank trends in order to identify regime changes that suggest the risk of a major equity market sell-off is high or, conversely, conditions are in place for a major equity market advance.

Market internals are essentially a swing vote that reinforces or dampens the primary message coming from the slow variables of market valuations and economic and central bank trends.

Market internals were downgraded to RED in early November due to deteriorating trend and momentum data. This is the first time market internals have been RED since March 2016.

Global Equity Market Trend Data as of March 1, 2019

| Sep | Oct | Nov | Dec | Jan | Feb | Mar | |

|---|---|---|---|---|---|---|---|

| Percentage of Global Markets Above 50 Day Moving Average | 32% | 49% | 17% | 25% | 21% | 92% | 83% |

| Percentage of Global Markets Above 200 Day Moving Average | 32% | 43% | 13% | 13% | 15% | 25% | 62% |

| Percentage of Global Stocks Above 50 Day Moving Average | 44% | 50% | 22% | 38% | 26% | 76% | 81% |

| Percentage of Global Stocks Above 200 Day Moving Average | 40% | 46% | 26% | 26% | 21% | 40% | 57% |

| Percent of Global Markets With Rising 200 Day Moving Averages | 51% | 47% | 38% | 19% | 15% | 17% | 23% |

Source: Ned Davis Research

Market internals improved in February and are back in YELLOW territory. Most stocks and markets are now trading above both their 50 day and 200 day moving averages. The percentage of global markets with rising 200-day moving averages improved to 23%.

Momentum measures the degree to which a market advance or market decline is accelerating or decelerating. There was some acceleration in January to mid-February, but recent momentum measures have peaked, albeit in neutral territory.

Shorter-term measures of investor sentiment reached levels of excessive optimism in February, but that has begun to reverse in the last week. The year-to-date market rally is notable in that inflows into equity mutual funds and ETFs have been meager, suggesting corporate buybacks and algorithms could be driving much of this market advance.

Summary

Global valuations, economic trends, and market internals are rated YELLOW. Overall investment conditions are low neutral. The risk of bad times is increasing as economic growth continues to slow, although not enough to push economic trends and overall investment conditions into RED territory.

This suggests investors should approach investing markets with caution. One could be more confident that the worse was behind us in terms of market losses if economic and earnings indicators were improving instead of deteriorating. Still, investment conditions remain YELLOW, in neutral territory, suggesting investors should be neither overly bearish or bullish. Investors should be patient (just like the Federal Reserve) in observing how investment conditions evolve in the coming weeks and months to determine whether they should be decreasing or increasing their portfolio risk.

The following tables provide a summary of market conditions by region.