Mortgage REITs pay some of the highest dividends in the world. How do mortgage REITs work and how can you invest in them?

What Are Mortgage REITs?

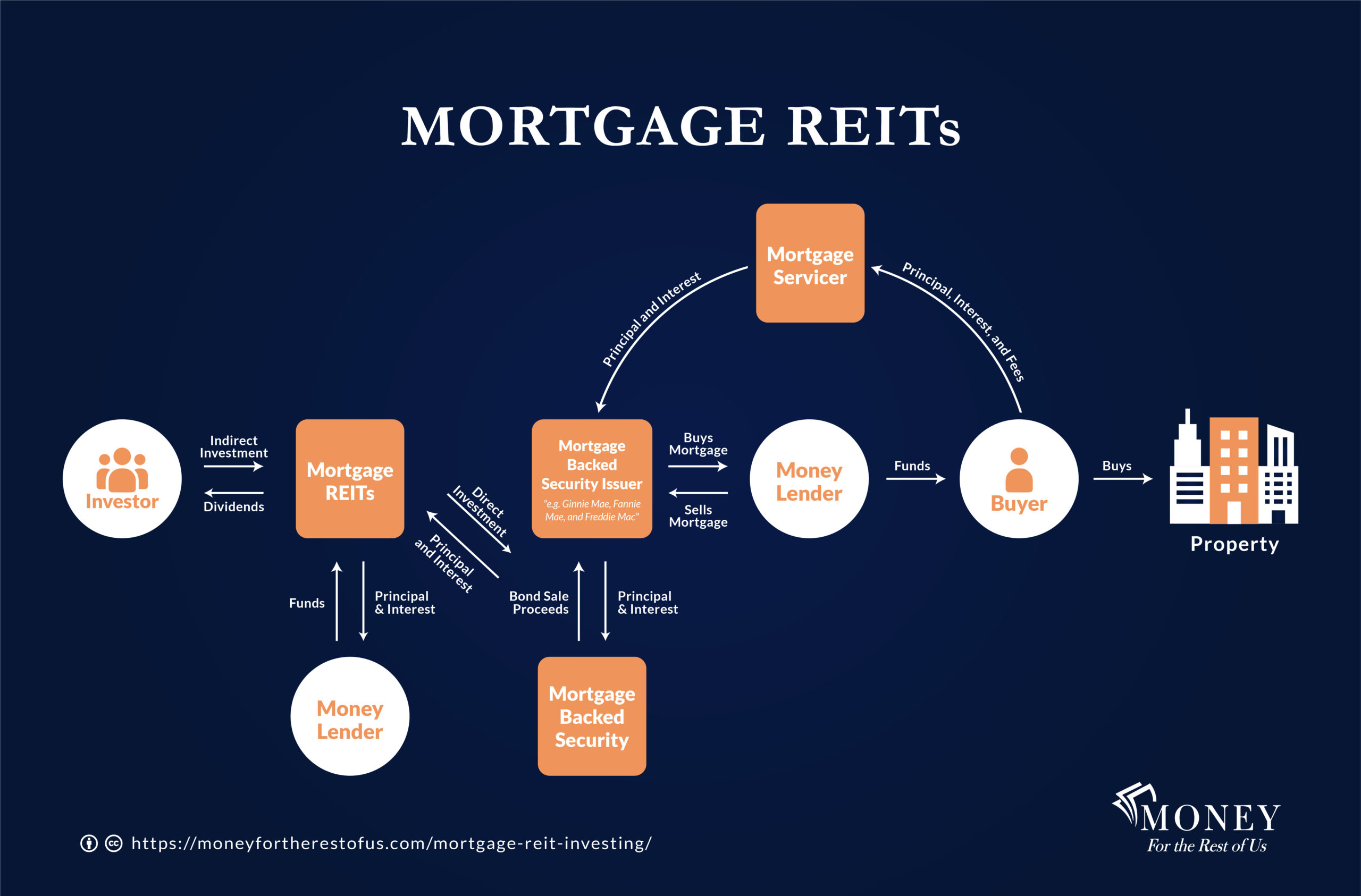

Mortgage real estate investment trusts are indirect investment vehicles that invest in residential and commercial mortgages. Mortgages are loans secured by real estate, such as houses, apartments, or office buildings.

Most mortgage REITs, also known as mREITs, invest in mortgages using mortgage-backed securities, a type of bond backed by a bundle of residential or commercial mortgages. Some mortgage REITs will also originate mortgages directly.

Mortgage REITs are indirect investment vehicles because a professional money management team selects the mortgages or mortgage-backed securities. The two largest mortgage REITs in the U.S. are Annaly Capital Management REIT (NLY) and AGNC Investment REIT (AGNC). Together they comprise just over 30% of the FTSE NAREIT All Mortgage Index, a benchmark that tracks mortgage REITs.

How Mortgage REITs Are Taxed

Similar to equity REITs that invest in income-producing real estate, mortgage REITs receive special tax treatment if they meet certain conditions set out by taxing authorities. These conditions vary by country. The main criteria to be classified as a REIT in the U.S. are:

- The REIT must be owned by more than 100 shareholders.

- The REIT must have more than 75% of its assets invested in real estate (including mortgages backed by real estate), government securities, or cash.

- 75% or more of the REIT’s gross income must be derived from real estate activities.

- At least 90% of the REIT’s taxable income must be distributed to shareholders as dividends.

If a U.S. REIT meets the requirements, it can deduct its dividend payments from its taxable income, which means REITs pay little if any income tax. Most corporations do not receive a tax deduction for dividends paid to shareholders, so these corporations pay dividends from after-tax income. REITs can pay higher dividend amounts than regular corporations because REITs pay dividends from pre-tax income.

Who Issues Mortgage-Backed Securities?

As mentioned, mortgage REITs primarily invest in bonds backed by residential and commercial mortgages. Most mortgage-backed securities in the U.S. are issued and guaranteed by government-sponsored enterprises or corporations owned by the federal government. Examples include the Federal National Mortgage Association, known as Fannie Mae, and the Federal Home Loan Mortgage Corporation, known as Freddie Mac.

U.S. Government Sponsored Enterprises and Agencies that Issue Mortgage-Backed Securities

Name

- Federal National Mortgage Association

- Federal Home Loan Mortgage Corporation

- Government National Mortgage Association

Nickname

- Fannie Mae

- Freddie Mac

- Ginnie Mae

These agencies purchase residential mortgage loans or pools of mortgage loans originated by qualifying financial institutions. The mortgages must meet specific lending standards and other criteria to be purchased.

Fannie Mae, Freddie Mac, and Ginnie Mae package these mortgages into bonds known as an agency mortgage-backed security or MBS. These bonds are called “pass-through securities” because the principal and interest that homeowners pay are passed on to the mortgage-backed security holders. Fannie Mae, Freddie Mac, and Ginnie Mae guarantee the payment of the principal and interest on the mortgages that comprise the agency mortgage-backed securities.

As of December 31, 2023, there was close to $12 trillion of U.S. agency mortgage-backed securities outstanding according to sifma.

In addition to mortgage-backed securities, Fannie Mae, Freddie Mac, and Ginnie Mae also issue interest-bearing bonds known as agency securities. The agencies use the proceeds from these bonds to fund their operations and to purchase mortgages that are eventually included in mortgage-backed securities.

These three agencies can issue debt at extremely low yields because investors assume the U.S. government will guarantee the performance of these bonds if Fannie Mae, Freddie Mac, or Ginnie Mae run into financial difficulties. This assumption proved correct during the Great Financial Crisis of 2008 and 2009 as the U.S. government did indeed provide financial assistance to these agencies and kept their bonds from defaulting.

Non-Agency Mortgage-backed Securities

Private issuers also package pools of mortgages into what are known as non-agency mortgage-backed securities. Non-agency mortgage-backed securities sometimes have insurance or other credit enhancements to protect holders from defaults on the underlying mortgages.

As of December 31, 2023, there was over $1.5 trillion of non-agency mortgage-backed securities outstanding, according to sifma.

How Mortgage REITs Work

Mortgage REITs primarily invest in agency mortgage-backed securities, although some will have exposure to non-agency mortgage-backed securities as well as mortgages or other lendings that they originate directly.

The interest rates on agency MBS tend to be low because the bonds are guaranteed by government agencies. Consequently, to pay out a high dividend, mortgage REITs use leverage by taking out debt and investing the proceeds in mortgage-backed securities.

Borrowing money to invest in an income-generating asset is known as a carry trade. The carry trade will be profitable as long as the interest rate on the debt is lower than the MBS yield and nothing happens that adversely impacts mortgage-backed security prices. The difference between the funding cost on the debt and the MBS yield is known as the net interest spread or net interest margin.

Become a Better Investor With Our Investing Checklist

Become a Better Investor With Our Investing Checklist

Master successful investing with our Checklist and get expert weekly insights to help you build your wealth with confidence.

Mortgage REIT Leverage

The primary debt source for mortgage REITs is repurchase agreements, which are also known as repos. Repurchase agreements are short-term collateralized loans. In a repo agreement, the mortgage-REIT sells its MBS holdings to a lender for cash and then promises to buy back the MBS later at a higher price. The MBS buyer earns interest, which is effectively the difference between the prices that the MBS was sold for and bought back. Essentially, the mortgage REIT borrows money to buy MBS and in turn, those securities serve as collateral for additional debt financing.

Mortgage REITs are highly leveraged in that the total debt can be ten times book value with book value being an entity’s total assets less liabilities, preferred stock, and intangible assets. Because leverage is so great, mortgage REITs will usually enter into hedging contracts in order to lock in the cost of their debt financing.

Hedging debt costs helps mortgage REITs have greater confidence that the net interest spread will be positive so that they can fund dividend payments to shareholders. The use of leverage allows mortgage REITs to magnify the yield on MBS and maintain dividend yields of over 10%.

Mortgage REIT Risks

The mortgage REIT carry trade will be profitable as long as the REIT can maintain a positive net interest margin or spread and the mortgage-backed securities that REITs hold don’t fall in price or even default in the case of non-agency mortgage-backed securities.

Mortgage REIT risks can be divided into risks that impact the net interest margin and risks that impact MBS prices. If these risks come to fruition, mortgage REIT profits fall, their book value declines, and dividends can be cut

Net Interest Margin Risks

Risks to the mortgage REIT net interest margin include a flattening yield curve and dislocations in the repo market.

Mortgage REITS benefit when longer-term interest rates that are used to determine mortgage rates are higher than short-term rates priced into repurchase agreements.

An upward sloping yield curve is when longer-term interest rates are higher than shorter-term interest rates. Mortgage REIT net interest spreads, and profits increase when there is an upward-sloping yield curve.

A flat yield curve is when short-term rates are similar to longer-term rates. An inverted yield curve is when short-term rates are higher than longer-term rates. When the yield curve is flat to inverted, mortgage REIT spreads are narrow, leading to reduced mortgage REIT profitability.

In early 2023, mortgage REITs net interest margins are narrowing because the yield curve is inverted, and prior hedges on borrowing costs are expiring, forcing mREITs to borrow at higher rates.

Mortgage REIT net interest margins can also be hit by a spike in debt costs, such as in September 2019, when there was a dislocation in the repo market caused by a supply-demand imbalance. Effectively the number of entities willing to lend in the repo market dropped, requiring borrowers to pay repo rates of up to 10%.

MBS Pricing Risks

Risks related to changes in MBS prices include interest rate risk, prepayment risk, and default risk.

Interest rate risk is the risk of rising interest rates that lead to falling bond prices. Like all bonds, mortgage-backed security prices decline when interest rates increase, harming the mortgage REIT. In 2022, a dramatic increase in interest rates caused the value of mortgage-back bonds to plummet. This led to a significant drop in mortgage REITs’ book values and well as their common stock share prices.

In addition, falling interest rates can also harm mortgage REITs. While MBS prices might increase a bit when interest rates decline, there is a limit to that increase because lower interest rates motivate homeowners to refinance their mortgages.

When a mortgage is refinanced, the principal payoff flows to the MBS that holds the mortgage. The amount received from the mortgage refinancing will often be less than the value of the mortgage reflected in the MBS because the mortgage value would have increased as interest rates fell. In other words, the mortgage will be marked at a premium, but the repayment will be at par value, which is the amount owed on the mortgage. That leads to a loss on that particular mortgage.

Prepayment risk represents the potential negative price impact of early mortgage payoffs. Prepayment risk increases when interest rates fall because more homeowners decide to refinance their mortgages.

Conversely, when interest rates rise, mortgage REITS could benefit from early mortgage payoffs because the payoff amount received could be greater than the current price of the mortgage within the MBS. Unfortunately for mortgage REITs, homeowners are less likely to refinance when interest rates increase.

Interest rate volatility increases prepayment risk as there is more potential for rates to fall and mortgage refinancings to increase.

Another risk to MBS pricing is the issuer’s default or defaults with the mortgages held by the mortgage-backed security. Agency mortgage-backed securities don’t have default risk because the issuers guarantee performance on the MBS and the underlying mortgages. Mortgage REITs that own non-agency mortgage-backed securities or that originate mortgages or other lending are exposed to default risk.

Risks to Mortgage REIT Shareholders

Due to the high leveraged employed by mortgage REITs, their share prices can fall sharply when net interest margin and MBS pricing risks increase as investors worry about mortgage REITs’ ability to sustain their dividend. Mortgage REITs that are not able to generate enough income per share to cover their existing dividend per share payment are forced to cut the dividend. Falling book values and the threat of dividend cuts have led to major losses for mortgage REITs in the past.

During the Great Financial Crisis (GFC) of 2008 and 2009, mortgage REITs fell 66% as measured by the FTSE NAREIT U.S. Mortgage REIT Index. It took eight years for mortgage REITs to recover the losses from the GFC fully. Mortgage REITs fell 57% during the spring of 2020 when the Covid-19 panic hit.

Mortgage REITs vs Equity REITs

Mortgage REITs

- Own mortgage-backed securities

- Receive interest income

- Highly leveraged

- High dividend yield

- Frequent dividend cuts

Equity REITs

- Own real estate

- Receive rental income

- Less leverage

- Lower dividend yield

- Infrequent dividend cuts

Mortgage REIT Historical and Expected Returns

Despite double-digit dividend yields, annualized total returns for REITs have fallen well short of that due to the periodic drawdowns that mortgage REITs experience.

Going back to 1972, the average rolling ten-year return for mortgage REITs has been 6.2% even though the average 10-year dividend yield is 11.3%. That means the average price return, which excludes dividends, has been negative for mortgage REITs. Mortgage REITs have not been able to recoup periodic drawdowns in their share prices due to falling book values and narrowing interest rate margins. On average mortgage REIT prices have fallen 4.4% annually.

For the ten years ending May 31, 2024, the FTSE Nareit All Mortgage REIT Index, a measure of mortgage REIT performance, returned 2.1% annualized. That is much lower than the 7.5% 10-year annualized return through December 31, 2021. The reason for the drop off in performance was a decline in mortgage REIT book values and common share prices in 2022 and 2023 as mortgage-backed securities declined due to rising interest rates.

A more predictable way to invest in mortgage REITs is by purchasing the preferred stock that mortgage REITs issue. Mortgage REIT preferred stock has a set dividend rate. Usually, the dividend rate is fixed but it can convert to a variable rate after the preferred shares have been outstanding for a number of years.

Mortgage REIT preferred stocks typically have fixed dividend rates of 6.5% to 8%. These dividends are cumulative so if a mortgage REIT is forced to suspend the dividend, it also has to suspend its common stock dividend. The preferred dividend accrues while it is suspended and has to be paid in full before the common stock dividend can be re-established.

How to Invest in Mortgage REITs

Investors can invest in individual mortgage-REITs common stock or invest in a mortgage REIT ETF like the iShares Mortgage Real Estate ETF (REM). Some mortgage REITs also offer preferred stock shares. Mortgage REIT preferreds pay out a lower dividend than the common shares. In theory, mortgage REIT preferreds should have lower drawdowns during market sell-offs. Still, they have fallen as much as the common shares because there are fewer preferred shares outstanding, so there is less liquidity, leading to large price declines during market sell-offs.

Investors can evaluate mortgage REITs by looking at their market price to book value per share. Mortgage REITs are more attractive when the common stock share price sells at a discount to the book value.

Another metric to consider is the mortgage REITs’ return on equity and its relation to the dividend yield. When the mortgage REIT return on equity is several percentage points higher than the dividend yield, the mortgage REIT has a buffer to incur some losses without cutting its dividend.

Finally, an investor can also look at the mortgage REITs’ dividend payout, which is the percentage of earnings a mortgage REIT pays as its dividend. When the dividend payout ratio is greater than 100%, that can be a sign of a potential dividend cut.

Pros and Cons of Mortgage REITs

Pros

- High dividend yield

- 6% annualized long-term return

Cons

- Complex

- Highly leveraged

- Frequent dividend cuts

Conclusion

Mortgage REITs are a high yielding, complicated asset class with a lot of moving parts. They are highly leveraged, and that leverage has led to volatility in the dividend, which has impacted mortgage REIT returns. While a double-digit dividend is attractive, the total returns for mortgage REITS have fallen short of the dividend yield with long-term annualized returns of 6%.

More risk-averse investors might find mortgage REIT preferred issues to be a better option because the returns have been similar to the common shares, but the dividend has been less volatile.

David Stein is the founder of Money for the Rest of Us. Since 2014, he has produced and hosted the Money for the Rest of Us investing podcast. The podcast reaches tens of thousands of listeners per episode and has been nominated for ten Plutus Awards and won one. David also leads Money for the Rest of Us Plus, a premium investment education platform that provides professional-grade portfolio tools and training to over 1,000 individual investors. He is the author of Money for the Rest of Us: 10 Questions to Master Successful Investing, which was published by McGraw-Hill. Previously, David spent over a decade as an institutional investment advisor and portfolio manager. He was a managing partner at FEG Investment Advisors, a $15 billion investment advisory firm. At FEG, David served as Chief Investment Strategist and Chief Portfolio Strategist.

Become a Better Investor With Our Investing Checklist

Become a Better Investor With Our Investing Checklist

Master successful investing with our Checklist and get expert weekly insights to help you build your wealth with confidence.