Convertible bonds are bonds that can be converted into shares of the issuer’s common stock. They’ve outperformed stocks over the past five years.

So how can you take advantage of convertible bonds and why would you want to?

What is a Convertible Bond?

Convertible bonds are debt securities issued by corporations that include an option for the holder to convert the bond into shares of the issuer’s common stock.

Convertible bonds, also called convertible notes, were first issued in the 19th century in the U.S. to raise capital to build out the railway system. Today convertible bonds are available worldwide with over $400 billion outstanding, although they remain a small subset of the overall corporate bond market. Convertible bonds comprise approximately 2.5% of the $8 trillion of U.S. corporate bonds outstanding.

Information technology companies are the largest issuer of convertible bonds, comprising over 30% of issues outstanding. About 60% of convertible bonds are denominated in U.S. dollars.

Why Companies Issue Convertible Bonds

Companies choose to issue convertible bonds because the interest rates are lower than on nonconvertible debt. This feature is attractive to companies with growing revenues that have yet to turn a profit.

Default risk is elevated for a company suffering losses, so bondholders demand higher interest rates. Using convertible bonds, a company can issue debt at a lower interest rate because investors get the protection of a senior debt security combined with the opportunity to participate in the company’s growth if its stock price increases.

Companies also issue convertible debt so they don’t have to go through the time-consuming process of having the bond issue rated by a credit rating agency.

Finally, convertible bonds allow companies to raise capital without immediately diluting existing common stock shareholders. Dilution means more common stock shares are outstanding, lowering the ownership percentage of each share. More common stock requires total earnings and dividends to be divided among more shares. Unless total earnings increase, when a company issues more stock shares, earnings per share could go down.

Eventually, when the convertible bonds are converted into stock, additional shares will be issued that dilute the common stock shareholders.

To delay the conversion, the stock price at which conversion makes economic sense for the convertible bondholder is typically at least 20% higher than the stock price when the convertible bond is issued.

How Do Convertible Bonds Work?

“Convertibles capture more return on the upside than on the downside.”

– Michael Youngworth, CFA, Vice President, Equity Derivatives Research at Bank of America Merrill Lynch

Similar to traditional bonds, convertibles pay interest, usually semi-annually, based on the coupon rate. On the maturity date, the bond’s par value, which is generally $1,000, is returned to the bondholder if the bond wasn’t converted into common stock.

Some convertible bonds can be redeemed or called early by the issuer, but the trend over the last decade is for most convertible bonds not to have a call feature. Convertible bonds that cannot be called usually have shorter maturities than those that can be called.

Convertibles are distinct from traditional bonds because the convertible bondholder has the option prior to the bond’s maturity to exchange the bond for a fixed number of common stock shares.

The conversion ratio is the number of common stock shares the bondholder will receive in exchange for the bond’s par value. The bond issue’s prospectus details the conversion ratio and other conditions that must be met for the bond to be converted into stock.

Most convertible bond issues contain a provision that increases the conversion ratio if the company pays a cash or stock dividend, issues additional stock shares, or there is a stock split.

The higher conversion ratio compensates the convertible bondholder for corporate events that increase the number of stock shares or puts downward pressure on the company’s stock.

How Convertible Bonds Are Analyzed and Priced

Convertible bonds have a fixed income component and equity component consisting of an option that gives a holder the right, but not the obligation, to convert the bond into stock.

Convertible bonds can be analyzed by separately evaluating the bond component and the equity component relative to the convertible’s market price.

A convertible bond’s investment value is its intrinsic value based on the bond’s fixed-income characteristics, such as prevailing interest rates, including the yield on the issuer’s nonconvertible bonds.

This investment value is a floor below which the convertible bond price rarely falls.

Most convertible bonds sell for more than the investment value. The difference between a convertible bond’s market price and its investment value is the investment premium.

This premium reflects the value investors place on the convertible bond apart from its role as an interest-bearing, fixed-income security.

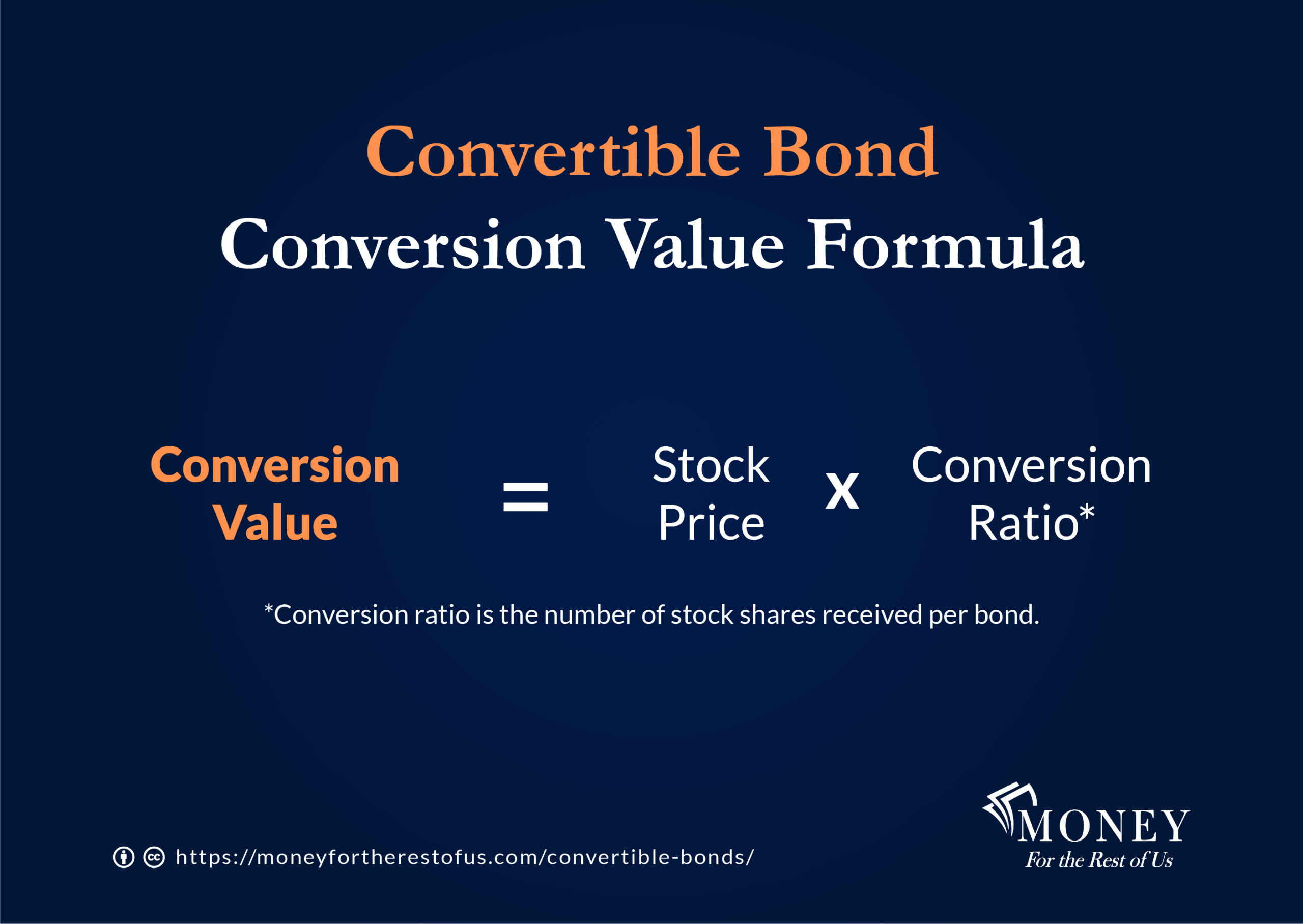

A convertible bond’s conversion value represents what the convertible bond is worth if it is converted into stock.

The conversion value is calculated by multiplying the stock price by the conversion ratio, which is the number of shares received per bond.

The conversion value is the minimum price a convertible bond should sell for when evaluating it from an equity perspective.

If the bond falls below the conversion value, investors could earn a risk-free profit through a strategy known as convertible bond arbitrage, described in more detail later in this guide.

Most convertible bonds sell for more than the conversion value. The difference between a convertible bond’s market price and its conversion value is the conversion premium.

The conversion premium is sometimes expressed as a percentage of the conversion value rather than the difference between them.

When a convertible bond’s conversion value is lower than the investment value, the convertible acts more like an interest-bearing bond. Its price fluctuates as interest rates change.

In this circumstance, the conversion premium is large, as the convertible’s market price is mostly determined by the convertible’s fixed-income characteristics. The reason is the stock price is too low to profitably exchange the bond for stock so the convertible trades more like a bond.

As the stock rises in price, the conversion value increases, and the conversion premium shrinks. When the conversion value exceeds the investment value, an investor can profitably convert the bond into stock. At this point, the convertible’s price is more volatile as it is closely tied to the issuer’s stock performance.

Convertible bonds whose conversion value is well below the investment value are known as busted converts. With busted converts, the investor consensus is that the stock price is unlikely to rise to a level in which exchanging the convertible bond into stock will be profitable.

Consequently, busted converts have low investment premiums and trade based on the bond’s fixed-income characteristics.

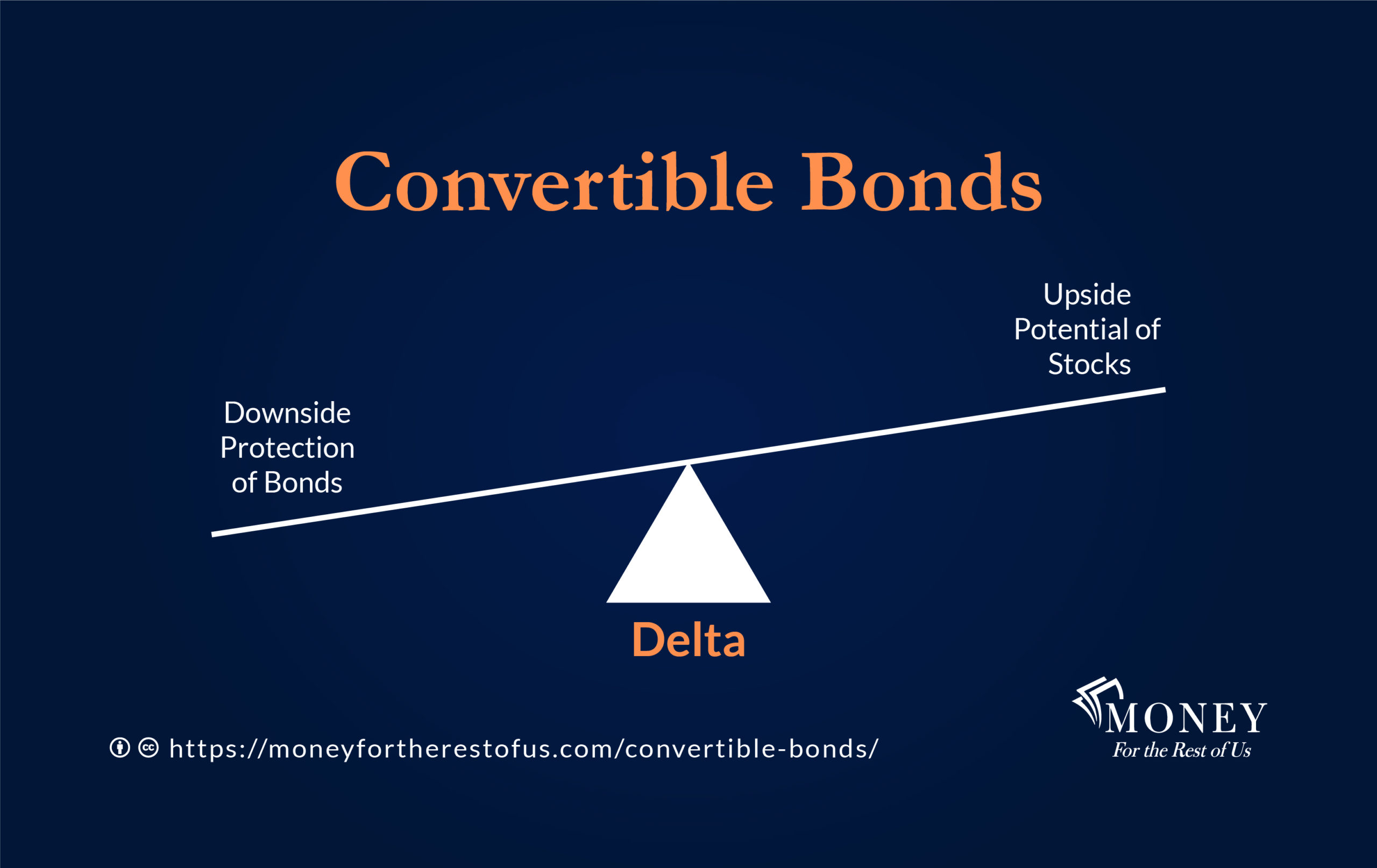

Delta is the measure used to calculate a convertible bond’s price sensitivity to its common stock. A convertible whose conversion value is well above its investment value will have a delta near one as the convertible bond’s price will fluctuate similarly as the stock price.

A convertible whose conversion value is well below the stock price will have a low delta as the convertible bond price will fluctuate like nonconvertible bonds.

The historical delta for major convertible bond indices such as the Thomson Reuters Qualified Global Convertibles Index is about 0.50, although the delta has gotten as high as 0.65 in 2007 and as low as 0.20 in 2009.

Convertible bonds are attractive because as the stock falls in price, the convertible bond’s fixed income component (i.e., its investment value), acts as a support level through which the convertible bond will not fall.

Likewise, as interest rates increase, convertible bonds often do not fall in price as much as nonconvertible bonds because of the convertible’s equity option.

There Are So Many Investing Books. Which One Is Worth Your Time?

Go beyond bestseller lists. Get a book recommendation from David based on your current interests, questions, and goals.

- Answer a few quick questions

- Based on your interests, not a generic bestseller list

- Built for curious, self-directed investors

- You’ll also get the Insider’s Guide newsletter for curated investing insights, podcast updates, and occasional offers

Convertible Bond Example

Tesla, the electric vehicle company, issued in May 2019 a 2% Convertible Senior Note that matures in 2024. Tesla’s stock price at the time was $244 per share. The conversion rate at issuance was 3.2276 shares of common stock per $1,000 par value of the bond.

The conversion value for Tesla’s convertible issue in May 2019 was $787.53. The conversion value is calculated by multiplying the 3.2276 conversion rate by the $244 stock price.

The conversion premium when the bond was issued was $212.47. The conversion premium is calculated by subtracting $787.53 conversion value from the $1,000 par value.

The conversion premium expressed as a percentage is 27%, which is calculated by dividing the $212.47 conversion premium by the $787.53 conversion value. At the time of issuance, Tesla’s stock price would need to increase by 27% for bondholders to break even when exchanging the bonds into stock.

By late 2019, Tesla’s stock price had risen to a level that it was profitable for investors to make the conversion. Since then, Tesla’s stock price has skyrocketed so that the convertible’s market price is significantly above the bond’s investment value and closely tied to the performance of Tesla’s common stock. The convertible’s delta is close to 1.

Convertible Bond Glossary

- Busted converts: Convertibles bonds where the conversion value is significantly lower than the investment value.

- Conversion price: The convertible bond par value divided by the conversion ratio.

- Conversion premium: The difference between the market price of a convertible bond and its conversion value.

- Conversion rate: The number of common stock shares the bondholder receives when exchanging a convertible bond.

- Conversion value: The convertible bond value if the bond is converted to stock. Calculated by multiplying the conversion rate by the stock price.

- Coupon rate: The annual interest rate paid on a bond.

- Delta: A measure of a convertible bond’s price relative to its common stock price. Jump to delta graphic.

- Investment value: The intrinsic price of the fixed income component of a convertible bond.

- Investment premium: The market price of the convertible bond less its investment value.

- Par value: The face value of the bond. Usually, it is $1,000.

Convertible Bond Arbitrage

Convertible bond arbitrage is a strategy that seeks to exploit mispricings between a convertible bond and its underlying stock. Most practitioners of convertible arbitrage are hedge funds, who are also the primary purchasers of convertible bonds.

An example of a convertible bond arbitrage strategy is buying the convertible bond while simultaneously selling short the stock. Short selling involves borrowing the stock shares and selling them.

Short sellers profit when a stock falls in price because the short sellers can repurchase shares at a lower price. By pairing a short sale with a convertible bond purchase, an arbitrager neutralizes stock price movements and earns a profit by collecting the convertible bond interest.

Convertible Bond Returns

The primary driver of convertible bond returns is the interest income based on the coupon rates and increases in conversion values as the underlying stock price increases.

Investors can estimate the return of a convertible bond index by taking its yield-to-maturity and adding an expected return for stocks multiplied by the estimated delta.

For example, if the yield to maturity is 1%, the estimated return for stocks is 6%, and the delta is 0.5, then the convertible bond estimated return would be 4% [1% + (6% x .5)]

Surprisingly, the U.S. convertible market has kept pace with the U.S. stock market as measured by the S&P 500 Index for the five years ending December 31, 2021.

The five year annualized return for the Bloomberg U.S. Convertible Cash Pay Bond > $250MM Index was 18.4% compared to 18.5% for the S&P 500 Index.

This strong performance was driven by tech-oriented companies such as Tesla which issued convertible bonds. Many of those companies have seen their stock prices jump, increasing the conversion value of their convertible bonds, which has driven the strong performance of convertible indices. This has pushed the delta of convertible bond indices closer to one.

Convertible Bond Risks

Like all bonds, convertible bonds are subject to default risk. Default occurs if the convertible bond issuer misses an interest payment or fails to return the principal balance. Historically, about 1% of convertible bonds default each year, which is lower than the default rate for non–investment grade bonds.

Convertible bonds are also subject to interest rate risk in that their prices can fall when interest rates increase.

Unlike other bonds, convertible bonds face equity risk. Convertibles fall in price when common stocks decline. Convertibles typically don’t fall as much as the stock market, but the asset class fell 32% both in 2008 and 2020.

How To Buy and Invest in Convertible Bonds

The most convenient way to purchase convertible bonds is through an indirect investment vehicle such as an exchange-traded fund (ETF), mutual fund, or closed-end fund.

An ETF will seek to match the performance of a particular convertible bond benchmark, while active mutual funds and closed-end funds seek to outperform the benchmark by selecting a subset of convertible issues outstanding.

Given Tesla’s sizable weight in convertible bond indices combined with its high delta, investors who want exposure to convertible bonds with a lower delta might consider mutual funds or closed-end funds that don’t hold Tesla’s convertibles.

Investors can also purchase individual convertible bonds through their brokerage accounts.

Convertible Bonds ETF Examples

- iShares Convertible Bond ETF (ICVT)

- SPDR Bloomberg Barclays Convertible Securities ETF (CWB)

Pros and Cons of Convertible Bonds

Pros

- Interest income

- Participation in stock market upside

- Downside protection from bond floor

Cons

- Complex

- Tesla’s oversized presence

Why Convertible Bonds Are Attractive To Investors

“Convertibles give investors the ability to generate equity-like returns with only a portion of the risk.”

– Tracy Maitland, president and CIO of Advent Capital Management

Convertible bonds are attractive investments because they allow investors to participate in the stock market’s upside with less downside because the bond attributes of convertibles act as a price floor.

An attractive time to purchase convertibles is after a significant stock market decline as conversion values and deltas are lower, allowing investors to benefit from the rebound in conversion values and deltas while having the downside protection of convertible’s investment value.

Podcast Episode 325: Convertible Bonds – The High Returning Asset Class That Vanguard Abandoned

Topics covered include:

- How big is the convertible bond market

- Why companies issue convertible bonds

- How convertible bonds work and how to analyze them

- Why convertible bonds have performed so well

- What is a reasonable expected return for convertible bonds and what are the risks

- What are ways to invest in convertible bonds

Show Notes

A Plunge and a Recovery Drives a Top-Performing Year in Convertibles by Andrew Bary—Barron’s

Convertible Bond Indices: An Overview by SPDR EMEA ETF Strategy Team—State Street Global Advisors

The Fluctuating Maturities of Convertible Bonds by Patrick Verwijmeren, and Antti Yang

Convertible Bond Arbitrage by George Long—Eureka Hedge

Episode Sponsors

Related Episodes

436: Revisiting Carbon, SPACs, Silver, Convertible Bonds, and Frontier Markets

Transcript

As a Money For the Rest of Us Plus member, you are able to listen to the podcast in an ad-free format and have access to the written transcript for each week’s episode. For listeners with hearing or other impairments that would like access to transcripts please send an email to jd@moneyfortherestofus.com Learn More About Plus Membership »

David Stein is the founder of Money for the Rest of Us. Since 2014, he has produced and hosted the Money for the Rest of Us investing podcast. The podcast reaches tens of thousands of listeners per episode and has been nominated for ten Plutus Awards and won one. David also leads Money for the Rest of Us Plus, a premium investment education platform that provides professional-grade portfolio tools and training to over 1,000 individual investors. He is the author of Money for the Rest of Us: 10 Questions to Master Successful Investing, which was published by McGraw-Hill. Previously, David spent over a decade as an institutional investment advisor and portfolio manager. He was a managing partner at FEG Investment Advisors, a $15 billion investment advisory firm. At FEG, David served as Chief Investment Strategist and Chief Portfolio Strategist.

Become a Better Investor With Our Investing Checklist

Become a Better Investor With Our Investing Checklist

Master successful investing with our Checklist and get expert weekly insights to help you build your wealth with confidence.