What is tail risk and how do you protect against it?

ARTICLE TABLE OF CONTENTS (Skip to Section)

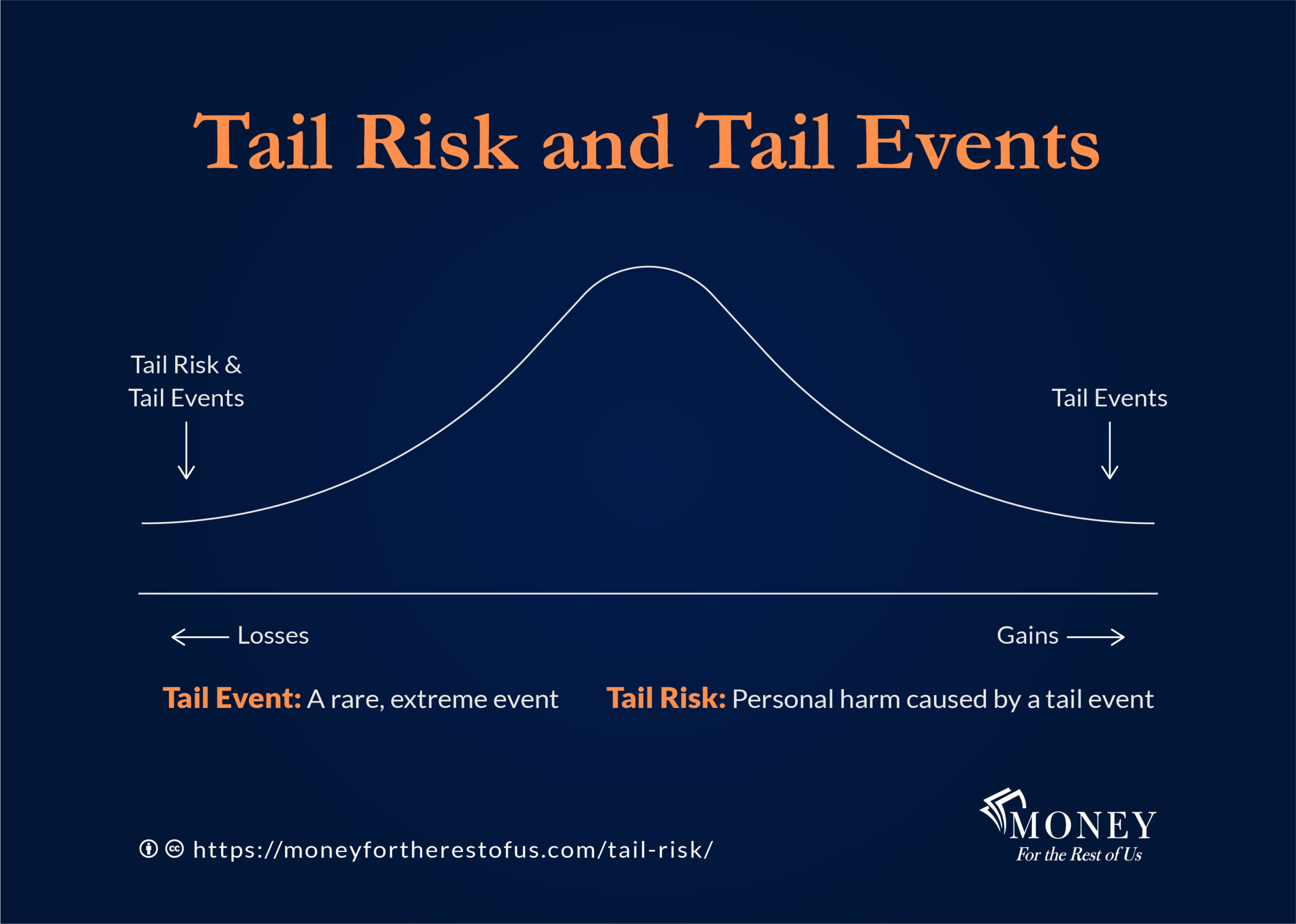

Tail Risk

Tail events are rare occurrences that are well outside of the norm. Tail risk is the personal harm caused by these tail events.

In the worst case, tail risk can ruin us. We could die. Or we could go bankrupt.

A Recent Weather Tail Event

In San Antonio, Texas, the average high temperature varies between 64 degrees and 96 degrees Fahrenheit in a typical year.

A plot of San Antonio’s daily high temperature would form a bell curve—what is known as a normal distribution. Most of the temperature observations cluster around the 70-degree mark.

There would be a few very cold temperature days plotted on the far left tail of the graph where the high temperature was in the teens and a few extremely hot temperature days of close to 110 degrees situated on the distribution’s far-right tail.

These extreme temperatures are the tail events.

For example, in February 2021, Texas was hit by a severe snow and ice storm. The high temperature was 29 degrees and the thermometer plunged to 10 degrees at night. That was the tail event.

Many powerplants, wind turbines, natural gas wells, and other power-generating infrastructure were unprepared for the extreme weather. They hadn’t sufficiently winterized.

As a result, 40% of Texas power generating capacity was off-line, unable to produce power while winter demand for power set a record.

Given the supply-demand mismatch, the Electric Reliability Council of Texas (ERCOT), which oversees the power grid in Texas, told electric utilities they needed to reduce demand by cutting the power to households and businesses. 2.8 million homes lost their power for hours at a time.

Numerous households suffered during the storm. Their houses were cold. Their pipes froze and burst. Unless these families had prepared by having an alternative energy source, they were exposed to the tail risk of well below normal temperatures given the failure of some power companies to prepare.

In addition, some households were exposed to the tail risk of electricity price surges when the wholesale cost of power jumped to $9,000 per megawatt-hour. These households had signed contracts in which they agreed to pay the wholesale cost of power rather than contracts where the average rate was more expensive but included a cap on what utility companies could charge.

How to Manage Tail Risk

Individuals and institutions have three options to manage tail risk.

- They can buy tail risk protection

- They can self-insure

- They can sell tail risk protection to others

When tail risk events can be identified beforehand and the probabilities of the event occurring can be estimated, then buying insurance is an effective way for individuals to protect against tail risk.

Insurance companies are experts at identifying the probabilities that an event will occur. Insurance companies aggregate a group of clients and charge them premiums to protect against specific events. Individual client premiums are set at a level that the total premium pool can compensate for client losses when the event occurs while still earning a profit for the insurance company.

Homeowners insurance, auto insurance, and health insurance provide peace of mind to individuals that they will not be financially ruined when a catastrophe occurs, such as a house fire or auto accident.

Protecting Against Stock Market Losses

Individual investors can get tail risk protection against severe stock market losses by purchasing put options or buying an ETF, such as the Cambria Tail Risk ETF (TAIL).

Purchasing tail risk protection against stock market losses can be expensive, costing between 1% to 7% per year depending on the level of losses the investor is seeking to avoid and the expected or implied volatility priced into options.

The measure of implied volatility for S&P 500 Index options is known as VIX. When the stock market’s expected volatility is high, then the cost to protect against stock market losses will also be high.

For younger investors, purchasing tail risk protection against stock market losses may not be worth the cost. These individuals have both the time and the earnings capacity from their employment to overcome stock market losses.

Become a Better Investor With Our Investing Checklist

Become a Better Investor With Our Investing Checklist

Master successful investing with our Checklist and get expert weekly insights to help you build your wealth with confidence.

Self Insurance Against Tail Risk

Stock market returns can be volatile, but the variability or volatility of stock returns is not the appropriate risk measure for many investors.

Rather, risk is the personal harm caused by extreme market losses.

For individuals that have years to retirement, a large stock market loss is unlikely to ruin them.

These individuals can self-insure against tail risk. They have a sufficient time buffer, financial reserves, and the ability to save more so that they can endure and overcome market losses.

Some businesses also self-insure against tail risk because they have sufficient financial reserves to pay any damages arising from extreme events. Of course, as we saw in the Texas storm, some businesses think they are prepared for extreme events, but in reality, they are not.

Selling Tail Risk Protection

Investors sell tail risk protection when they sell or write put options. These investors receive a premium for selling the option, just like insurance companies receive compensation for selling insurance.

In addition, the option seller has the obligation to purchase the stock or ETF detailed in the option contract if it falls below a specific price known as the strike price.

Investors who sell put options will be on the hook for losses that occur when the stock, ETF, or other financial security falls below the strike price. Those losses will offset any premium that was earned.

The WisdomTree CBOE S&P 500 PutWrite Strategy ETF (PUTW) is an ETF that sells tail risk protection.

The ETF sells put options that expire in 30 days at the current level of the S&P 500 Index. The ETF receives the premium for selling the put options, but if the S&P 500 Index falls in price during the month, the ETF will incur the losses.

Since its inception in February 2016, WisdomTree CBOE S&P 500 PutWrite Strategy ETF has returned 5.8% annualized.

A 5% to 7% return is a reasonable return expectation for strategies that sell put options.

Reserves to Protect Against Uncertainty

Some tail events cannot be identified beforehand and therefore the probabilities can’t be estimated. These are uncertain events. This guide explains the differences between risk and uncertainty in more detail.

We protect against uncertainties by building a margin of safety. These buffers include having emergency savings, a financial reserve, extra food, water, and an alternative source of power.

By having buffers and reserves, we can prepare for the unexpected without having to predict when or what tail event may happen.

Podcast Episode 332: What Is Tail Risk and Are You Taking Too Much Of It?

When should you protect against rare, but extreme events? When should you self-insure? Under what circumstance should you sell tail risk protection to others?

Topics covered include:

- How tail events differ from tail risk

- Why volatility is not the best measure of risk for individuals

- What does it cost to protect against large stock market losses

- Why younger investors can take more risk due to their human capital

- How does the profit wheel options strategy work

- How the catastrophic power outage in Texas exemplifies tail risk

- Why individuals need to build more reserves because the economic system is too efficient and vulnerable to breakdowns

Show Notes

Average Weather in San Antonio Texas, United States—Weather Spark

Update on the CBOE BuyWrite and PutWrite Option Indexes, October 2018—Asset Consulting Group

The Texas Freeze: Why the Power Grid Failed Katherine Blunt and Russell Gold—The Wall Street Journal

When More Is Not Better: Overcoming America’s Obsession with Economic Efficiency by Roger L. Martin

Episode Sponsors

Related Episodes

250: Investing Rule One—Avoid Ruin

283: Why You Should Care About Carry Trades

321: How to Analyze Complex Investments

323: The Economy Is Not A Machine

354: Now Is the Best Time Ever to Be an Individual Investor

377: What If It’s Different This Time? – The Impact of the Russian-Ukraine War

Transcript

As a Money For the Rest of Us Plus member, you are able to listen to the podcast in an ad-free format and have access to the written transcript for each week’s episode. For listeners with hearing or other impairments that would like access to transcripts please send an email to jd@moneyfortherestofus.com Learn More About Plus Membership »

David Stein is the founder of Money for the Rest of Us. Since 2014, he has produced and hosted the Money for the Rest of Us investing podcast. The podcast reaches tens of thousands of listeners per episode and has been nominated for ten Plutus Awards and won one. David also leads Money for the Rest of Us Plus, a premium investment education platform that provides professional-grade portfolio tools and training to over 1,000 individual investors. He is the author of Money for the Rest of Us: 10 Questions to Master Successful Investing, which was published by McGraw-Hill. Previously, David spent over a decade as an institutional investment advisor and portfolio manager. He was a managing partner at FEG Investment Advisors, a $15 billion investment advisory firm. At FEG, David served as Chief Investment Strategist and Chief Portfolio Strategist.

Become a Better Investor With Our Investing Checklist

Become a Better Investor With Our Investing Checklist

Master successful investing with our Checklist and get expert weekly insights to help you build your wealth with confidence.