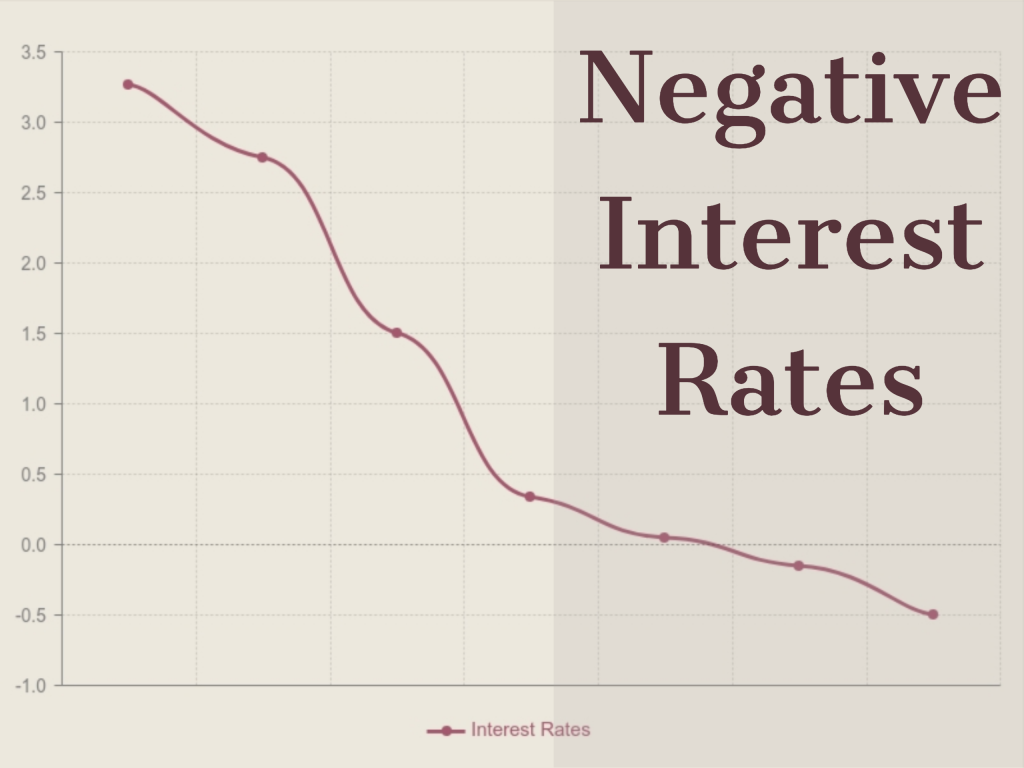

Recently, the yield on the 30-year government bond in Germany went negative for the first time ever. Now there are 15 trillion dollars of bonds around the world, about 25% of the world’s bond supply that are priced so they earn a negative yield. That effectively means that investors are paying someone to hold their money. That there’s a cost to actually investing.

The Math Behind Negative Yielding Bonds

Most bonds that have a negative yield were not issued with a negative interest rate. Instead, investors bid up the bond price to such a high level that after factoring in the interest payments and the return of principal, investors have a negative return. For example, suppose an investor pays $105 for a bond that was originally issued at $100 and that bond pays interest at 1% per year. The bond matures in two more years so the investor will receive $2 of interest and $100 in principal when the bond matures. That means the investor paid $105 and only received $102 in return. The return was negative.

Some countries have actually issued bonds that have a negative yield. In March of 2019, Germany sold 2.4 billion euros of 10-year government bonds at an average yield of -.05%. The German government received 2.6 times more bids for the debt than what was accepted.

Even in that case, the stated interest rate was 0% and demand for the bond pushed up the issue price so it had a negative yield. Currently, there is not the infrastructure in place for governments to issue bonds that have a negative interest rate. Such bonds would require the investor to make interest payments to the government.

Three Reasons to Buy A Negative Yielding Bond

There are three reasons why investors are willing to buy a negative-yielding bond that is guaranteed to lose money if held to maturity.

1. Interest Rate Speculation

First, investors might buy negative-yielding bonds because they believe interest rates will fall further. Under that scenario, the investors benefit from the capital appreciation because as interest rates fall, the price of bonds goes up. If interest rates are negative when investors buy a bond and interest rates become more negative, then the price of the bond went up by even more. That means investors could lock in a profit if they sold the bonds.

2. Rolling Down the Yield Curve

A second reason to buy negative-yielding bonds is to benefit from a concept called rolling down the yield curve. Even if there isn’t any change in interest rates, investors can earn a little bit of profit as bonds get closer to maturity if longer-term interest rates are higher than shorter-term rates.

For example, investors who buy a 10-year bond will be holding a 9-year bond after one year due to the passage of time. If 9-year bonds are priced to have a lower yield than 10-year bonds, investors could earn a small profit.

Since 2016, a period when 7 to 10-year Japanese government bonds have had a negative yield, the overall return for those bonds has been 0.46% annualized. Investors got a little bit of price appreciation as the 10-year bonds became 9-year bonds, became 8-year bonds, became 7-year bonds.

3. Safekeeping Capital

The third reason to own a negative-yielding bond is as a safe place to store money. Some investors want the security of keeping a portion of their capital in high-quality government bonds even if it cost them a little bit to do so. Often these investors have huge amounts of money where it is not practical to place it with a bank due to monetary limits on deposit insurance. Balances above some monetary threshold would not be reimbursed by the government if the bank fails. Instead, investors with large sums of money can store their capital in the extremely liquid government bond market, perhaps while they wait for more attractive investment opportunities to come along.

These three reasons show that even in negative-yielding bonds seem irrational, there are actually some rational reasons to invest in them.

To learn more about negative interest rate and what to do about them, please listen to this episode of Money For the Rest of Us.

Topics covered include:

- How negative interest rates are even possible.

- How longer life spans, central bank actions, changing time preferences, and the FIRE movement are contributing to negative interest rates.

- What is the paradox of thrift.

- How investors can earn a positive return on bonds even if interest rates are negative.

- What are some indicators to watch for that could signal imminent negative interest rates in the U.S.

- How individuals need to adjust their lifestyles in an era of negative interest rates.

Show Notes

Personal Saving Rate—Federal Reserve Bank of St. Louis

How Interest Rates Affect Time Preference — and Vice Versa by Frank Shostak—Mises Institute

Austrian School of Economics By Peter J. Boettke—The Library of Economics and Liberty

Interest Rates: Naturally Negative? by Joachim Fels— PIMCO Blog

How This Bull Market Will End by Randall W. Forsyth—Barrons

Episode Sponsors

Become a Better Investor With Our Investing Checklist

Become a Better Investor With Our Investing Checklist

Master successful investing with our Checklist and get expert weekly insights to help you build your wealth with confidence.

Episode Chronology

- [0:20] Germany’s government bonds go negative for the first time.

- [2:38] Understanding savings: the paradox of thrift.

- [6:35] The concept of the individual choice and the perceived expense of saving.

- [11:05] The savings glut could lead to negative interest rates in the U.S.

- [14:40] Three reasons one would invest in negative-yielding bonds.

- [18:38] Central banks are influencing the spread of negative-yielding bonds.

- [20:29] What could happen to the U.S. economy if interest rates fell.

- [22:11] Three factors David is looking at for an indication of falling interest rates.

- [25:49] What we can do if U.S. interest rates go negative.

Related Episodes

22: Will Interest Rates Ever Increase?

52: Why Are Interest Rates So Low, Even Negative In Some Places

82: What Assets Return When The Fed Raises Rates

122: Why Negative Interest Rates Are Dangerous

133: Interest Rates Are Rising. Four Things You Can Do

255: With Interest Rates Falling, Why Do You Own Bonds?

260: Is This Why Interest Rates Are Falling and the Global Economy Slowing?

308: Coins and Cash: Shortages, Hoarding, and Threats

Transcript

Welcome to Money for the Rest of Us, this is a personal finance show on money, how it works, how to invest it and how to live without worrying about it. I’m your host David Stein. Today is episode 264. It’s titled “What Happens If U.S. Interest Rates Go Negative?”

Negative German bonds

Last week the yield on the 30-year government bond in Germany went negative for the first time ever. Now there are 15 trillion dollars of bonds around the world, about 25% of the world’s bond supply that are priced so they earn a negative yield. That effectively means that you’re paying, when you buy one of these bonds, you’re paying somebody money to hold your money. There’s a cost to actually investing.

Back in episode 225, it was how to invest in bonds, and we talked about the relationship between interest rates and bonds. As interest rates go up, the value or the price of bonds fall. And when interest rates fall the price of bonds go up.

In order for a bond to have a negative interest rate, for bonds that are actually outstanding already. Let’s say it’s originally a German bond, a 10-year bond, that was priced to yield 1% and is paying interest of 1%. If rates fall enough the price of that bond goes up so high that when you factor in the interest payments you’re receiving plus the principle that you receive. Let’s say at the end of the bond you get $100 of the principal back, but you paid $120 to buy the bond, then you’re going to effectively have a loss.

But it’s not just that. The German government is actually issuing new bonds that have a negative yield. In March of 2019, there was an article in the Financial Times that mentioned Germany had sold 2.4 billion euros of 10-year government bonds at an average yield of -.05%. They said that they received 2.6 times more bids for the debt that was accepted. Financial Times clarified the negative yield means that investors who bought at Wednesday’s auction and hold to maturity are guaranteed to sustain a loss. That was back in March. Now we’re in August and the yield on 10-year government paper is -0.6%.

What drives negative interest rates and is it possible that we could have negative interest rates in the U.S.? What would that mean for our retirement savings? What would that mean for the economy? We’re going to take a look at that in today’s episode.

Understanding savings

To better understand why interest rates are negative in many parts of the world, we need to understand savings, how savings work. The measure of savings in the U.S. is known as the personal savings rate, and it measures how much to save as a percentage of disposable personal income. Disposable personal income is the income an individual has after paying taxes, and then what percentage of that after-tax income is saved.

This rate started dropping after the 1991-1992 recession. In December 1992 the personal savings rate was 10.6%. By July 2005 it was 2.2%, the lowest ever. Right before the Great Financial Crisis started, November 2007, the personal savings rate was 3.1%. Now it’s 8.1%. It’s been creeping up. People are saving more.

As a Money For the Rest of Us Plus member, you are able to listen to the podcast in an ad-free format and have access to the written transcript for each week’s episode. For listeners with hearing or other impairments that would like access to transcripts please send an email to jd@moneyfortherestofus.com Learn More About Plus Membership »